Macro Overview

The rally in stocks that began following the election in 2016 propelled through 2017 as optimism and expectations that growth oriented policies and tax cuts would materialize. Political turmoil was not a deterrent for the markets, as major U.S. equity indices finished the year at near record levels.

The Tax Cut & Jobs Act was signed into law by the President on December 22nd, setting the stage for new tax codes and rules effective January 1, 2018. Following the passage of the new tax law legislation, small businesses and larger corporations prepare for optimal methods of spending capital and expanding in 2018.

Congress passed a short-term funding plan to avert a government shutdown between December 22nd to January 19th. Since federal funding gaps are common, Congress institutes a continuing resolution or CR to provide interim funds in order to maintain government operations.

Strengthening economic conditions throughout the international markets helped buoy global stocks and mildly boost inflationary pressures, which can be beneficial for certain equities. Economic stimulus efforts by central banks were reigned in during 2017, as developed and emerging market economies exceeded growth expectations.

The Federal Reserve raised rates as expected with the objective of curtailing inflationary pressures. The December rate hike was the third of the year, pushing shorter-term rates higher, which are more sensitive to Fed rate increases. Overall, rates remained fairly stable in 2017, as inflation and economic growth were tepid. The 10-year Treasury yield ended 2017 at 2.40%, down from 2.45% at the beginning of the year.

Commodity prices, including precious metals and energy products, are expected to rise in 2018 as the prospect of inflationary pressures increases. A rise in global oil demand along with curtailment of production pushed prices higher in 2017 to levels not reached in over two years.

Confusion surrounding prepayment of property taxes was a nationwide problem the last week of the year as homeowners rushed to prepay 2018 property tax bills without being certain if a deduction could be taken in 2017. In a statement, the IRS did specify that taxpayers could deduct prepaid 2018 state and local property taxes on 2017 returns only if the taxes were assessed before 2018.

Sources: Congress.gov, Federal Reserve, IRS, U.S. Treasury

Equity Overview – Global Stock Update

Global markets accelerated throughout 2017, marking new highs and sending broader market indices higher. The election prompted rally in domestic stocks continued on in 2017 as optimism and expectations that growth oriented policies and tax cuts would fuel earnings appreciation.

International markets excelled in 2017 as both developing and emerging stocks were boosted by expanding economies throughout Europe and Asia.

The new tax law imposes a repatriation tax on cash held overseas by U.S. corporations. A tax of 15.5% on liquid assets will affect various sectors and numerous companies that are estimated to have amassed over $2 trillion overseas. The new rate is considerably lower than the previous rate of 35%, incentivizing companies to bring cash back to the U.S.

Of the several sectors encompassing the equity markets, technology and healthcare companies hold the most cash overseas, placing them at the forefront of bringing billions of dollars back to the U.S. at the preferable tax rate.

Sources: Bloomberg, Reuters, www.congress.gov/bill/115th-congress/house-bill/1

Short Term Rates Heading Higher – Bond Market Overview

The Federal Reserve raised a key short-term rate as expected by the markets and made fairly optimistic comments about economic growth projections for 2018. The federal funds rate rose to a target range of 1.25 – 1.50%. The increase is a strategy of tightening and also meant to alleviate inflationary pressures. Concurrently, the Fed is also shrinking its $4.4 trillion balance sheet, a dual monetary policy effect expected to curtail inflation and reduce stimulus.

Members of the Federal Reserve indirectly expressed concern about the labor market, suggesting that improvements in the job market were expected to ease. The Fed committee also maintained a conservative growth estimate for 2018 of 1.8%, hinting that the new tax plan may not yet produce economic benefits in 2018.

The yield curve flattened throughout 2017, with a rise in short term rates and a drop in longer-term rates. The yield on the 2-year Treasury Note had its largest annual increase in over 10 years, ending the year at 1.89%, up from 1.22% at the beginning of January 2017. The benchmark 10-year Treasury bond yield saw almost no change in 2017, falling to 2.40% at year end from 2.45% in the beginning of January.

The current Chair of the Fed, Janet Yellen, is scheduled to chair her last Fed meeting on January 30th & 31st, with Jerome Powell assuming the post in February.

Sources: Federal Reserve, U.S. Treasury, Bloomberg

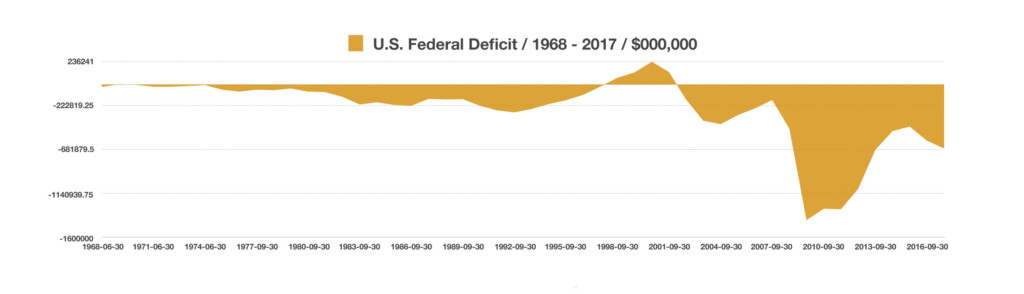

Deficit History & Tax Cuts – Fiscal Policy

The passage of the Tax Cuts & Jobs Act has prompted a flurry of analysis and criticism surrounding the affects on the Federal deficit due to lower tax revenue. Critics claim that the loss of tax revenue due to tax cuts will eventually lead to an increase in the Federal deficit unless economic growth is achieved.

The affect on individuals should the deficit grow is that the cost to borrow for the U.S. government would go up, thus leading to an increase in interest rates for consumers. So as the shortfall in receipts rises it also becomes more expensive for the government to carry debt (interest payments) because rates have risen.

Historically, rising deficit levels have brought about inflation as the Federal government issues more debt to sustain it’s spending abilities following tax revenue losses.

Deficits can get larger from fiscal policy reform, such as tax cuts or government spending increases, and also increase during poor economic periods. The federal deficit grew very quickly following the financial crisis of 2008-2009 as tax revenue fell sharply. Conversely, prior deficits have also shrunk as economic growth has led to tax revenue increases.

Sources: GAO, Federal Reserve; fred.stlouisfed.org/series/FYFSD

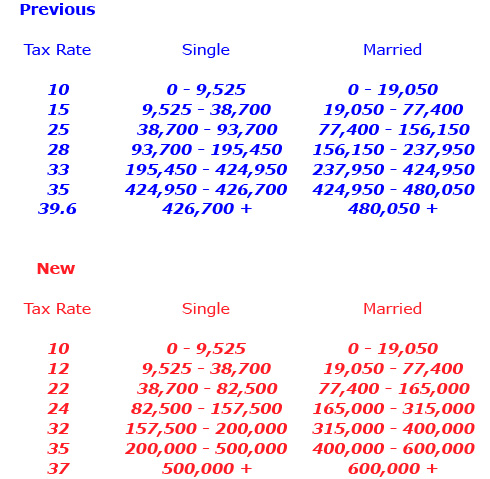

The New Tax Bill – Fiscal Policy Review

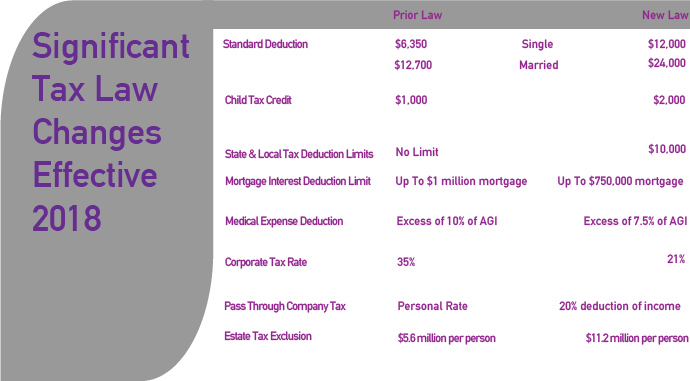

Both individual taxpayers and companies will see broad changes for deductions and tax rates. The emphasis of the tax bill, known formally as the Tax Cuts & Jobs Act, is to stimulate economic activity via new and higher paying jobs. This is why many of the changes directly benefit large and small businesses in order to encourage hiring.

Some of the tax provisions enacted by the new tax act will be temporary, while others permanent. The cost of reduced tax revenue brought about by tax cuts may only be viable for a certain period, thus producing more immediate benefits from tax cuts rather than later.

Affecting essentially every taxpayer is the increase in the standard deduction, which is meant to simplify the tax preparation process by replacing itemized deductions with a larger standard deduction.

The IRS estimates that about 95% of the businesses in the United States are pass-through entities, such as sole proprietors, S-Corps, LLCs, and partnerships. These entities are called pass-throughs because the profits generated are passed directly through the business to the owners, which are taxed at the owners’ individual income tax rates. The new tax law allows for a 20% deduction of that income, thus reducing overall taxable income. According to the Tax Foundation, pass-through businesses account for over 55% of all private sector employment, representing over 65.5 million workers nationwide.

Sources: IRS, www.congress.gov/bill/115th-congress/house-bill/1,

New Rules Benefit 529 College Savings Plans As An Estate Tool – Estate Planning

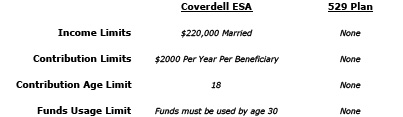

The Tax Cuts and Jobs Act includes a provision to now allow 529 Plans to be used for private elementary and high school expenses, rather than just college related expenses. The new rules are a treat for both parents and grandparents looking for a better way to pay for private educational costs.

Until now, the only plan that allowed for tax-free earnings growth was a Coverdell Education Savings Account (ESA). Limitations on contributions and income has made these plans unfavorable for many families.

A key notable benefit to a 529 versus a Coverdell ESA includes transferability. Funds in a 529 account may be transferred from the original beneficiary to another. Another benefit is the fact that funds in a 529 may grow perpetually, and never have to be used. Some families are using this feature as an estate planning tool, allowing unused funds in a 529 to pass along to future recipients.

The new tax plan does limit the amount used for K-12 expenses to $10,000 per year. Any current funds held in an existing Coverdell ESA account may be rolled over to a 529 plan with no tax consequences.

Named after the IRS Code it falls under, Section 529 plans have ballooned to $282 billion in assets (as of the 3rd quarter of 2017) since their inception in 1997. Section 529 plans were initially intended to provide parents of young children the ability to invest money for future anticipated college related expenses.

These plans offer two primary benefits: assets grow tax deferred and come out tax free for qualified expenses; and, contributions made by parents and grandparents are considered a gift, thus proving a tax benefit for some contributors.

Source: IRS, www.congress.gov/bill/115th-congress/house-bill/1

*Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.