Macro Overview – Sept 2018

Trade and tariffs continued at the forefront of discussions among the U.S. and international trading partners. Topics at hand included the North American Free Trade Agreement (NAFTA), the World Trade Organization (WTO), and protecting U.S. intellectual property rights internationally.

Emerging market currencies were rattled worldwide as turmoil with Argentina and Turkey spilled over into the broader markets. Contagion concerns spread in late August as Turkey’s currency fell following comments by the European Central Bank (ECB). Argentina saw its currency collapse as it sought immediate financial assistance from the International Monetary Fund (IMF). Contagion refers to the threat of what is occurring in Turkey and Argentina could migrate to other emerging market economies. The brewing financial crisis with Turkey is similar to the government debt crisis that occurred with Greece eight years ago. Recently imposed U.S. sanctions on Russia added to emerging market distress as the Russian ruble weakened versus other major currencies and the U.S. dollar.

The stock market marked its longest period of uninterrupted gains in history, running 3,453 days from the market low on March 9, 2009 during the depths of the financial crisis. Since then, the Dow Jones Industrial Index catapulted from 6,500 to over 25,500 in August, while the S&P 500 sprang from 666 to over 2800. Many economists and market analysts attribute the tremendous run to Fed induced liquidity in the form of ultra low rates for an extended period of time.

It has been 10 years since the financial crisis of 2008 when financial markets experienced turbulence not seen in decades. An ultra low interest rate environment ensued for nearly a decade after the Federal Reserve began flooding the financial markets with massive amounts of liquidity in order to stem the crisis at hand. Since then, numerous legislation and regulations were implemented providing safety measures and guidelines.

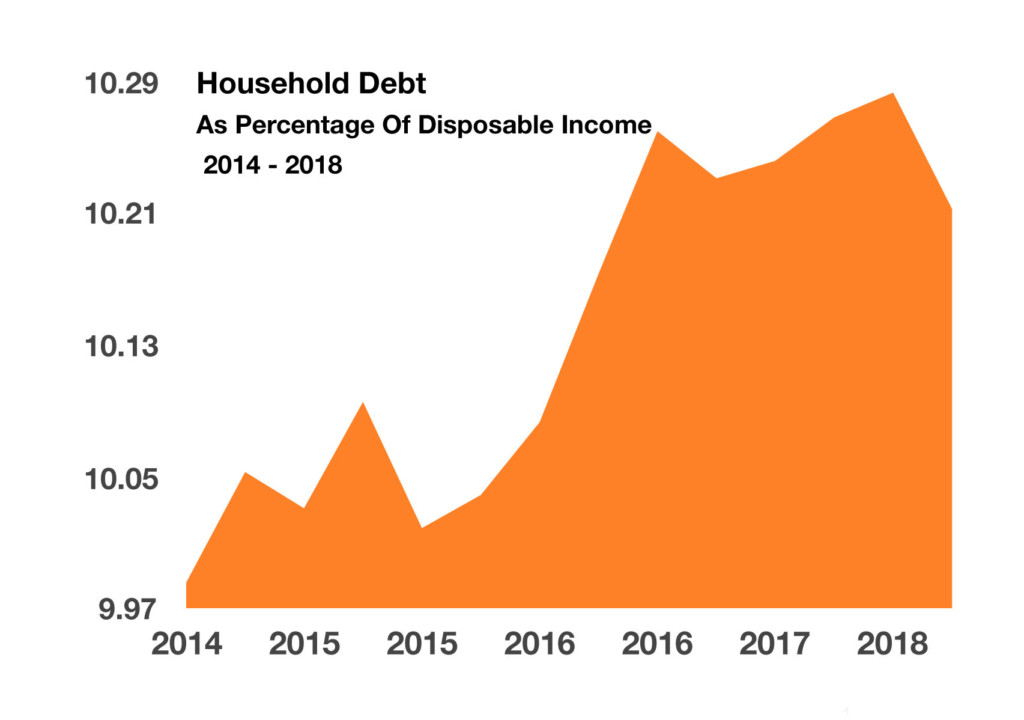

Viewed as an optimistic indicator for the U.S. economy, inflation rose the most in seven years as consumer prices increased at an annual rate of 2.9%. While inflation is an indicator of economic expansion in the economy, wages are not keeping up with rising prices nationwide.

California is due to become the first state to impose a quota for the inclusion of women on the boards of publicly traded companies headquartered in the state. Other states are expected to follow California’s lead by eventually implementing similar mandates.

Various social media and technology companies are facing criticism and possible regulatory oversight regarding the influence they maintain. Many see that the political and cultural clout held by just a few companies may eventually be of concern.

Sources: ECB, IMF, Dept. of Commerce, Bloomberg, http://www.leginfo.legislature.ca.gov

Equities Maintain Their Resilience - U.S. Equity Markets

A persistent trade dispute between the United States and China has been lingering over the financial markets for some time now. Helping to buoy domestic markets are strong corporate earnings and improving economic data. Earnings from U.S. companies this quarter are being considered the healthiest since the third quarter of 2009 during the financial crisis.

Some U.S. companies are seeing an increase in sales as well as an increase in gross margins, considered optimistic by equity analysts. The continued strength of the U.S. dollar, however, is starting to weigh on earnings for certain companies transacting business overseas.

The administration has proposed altering quarterly reporting for publicly traded U.S. companies to a semi-annual basis. Similar proposals have been made by companies and regulators in the past in order to stem volatility and focus on earnings. Recent news has focused on some companies going private and shedding the regulatory hurdles and burden caused by quarterly reporting.

Sources: Bloomberg, Federal Reserve Bank of St. Louis

Yields Continue To Flatten - Fixed Income Update

A flattening Treasury yield curve remained a focal topic among fixed income analysts in August. The shrinking spread, or difference, between the yield on the 2-year Treasury note and the 10-year Treasury bond reached levels not seen since 2007. The interpretation is that longer term economic growth is expected to be muted, which is reflected in the yield of the 10 year Treasury. The Federal Reserve is still on course for additional rate hikes, but at a very gradual pace.

Ten years have passed since the financial crisis that began in September 2008 when the Federal Reserve flooded the financial markets with massive amounts of liquidity in order to stem the crisis at hand. An ultra low interest rate environment followed for nearly a decade before the Fed reversed course and started raising rates once again.

The Federal Reserve mentioned during one of its meetings in August that it had determined when a prolonged period of low volatility exists, an increase in lending and risk-taking ensures.

Sources: U.S. Treasury, Bloomberg

Emerging Market Currencies Experience Volatility - International Currency Review

Currency valuations across the emerging markets are being affected by recent financial turmoil in Turkey and Argentina. The Turkish currency, the lira, has fallen over 40% year to date versus the U.S. dollar. The Turkish lira has been the hardest hit so far this year of all of the emerging market currencies. Emerging market currencies, as tracked and measured by the MSCI International Emerging Market Index, has had a continuous decline since the beginning of 2018.

Concerns about the exposure that European banks have to Turkish bonds became a forefront topic for global bankers. Government spending by Turkey has been equal to that of the government in Greece that led to the country’s debt crisis in 2012. Circumstances that occurred in Greece are appearing in Turkey as mounting government debt has hindered the government’s finances and integrity.

The Argentine peso has lost over half its value versus the U.S. dollar so far this year. A sell-off in the Argentine currency was exacerbated when the president of Argentina asked the International Monetary Fund to speed up its release of $50 billion in bailout funds for the country.

Ironically, the economic growth and strength of the U.S. dollar has been a catalyst for emerging market currency turmoil. The problem lies with dollar denominated debt owed by emerging market countries such as Turkey, Greece, Argentina, and Venezuela. As the U.S. dollar appreciates versus the currencies of these other countries, the cost to repay the debt increases.

Large international banks and institutional holders of emerging market debt buy insurance to protect themselves from default, should countries become unable to pay their debt. The insurance is known as credit default swaps or CDSs. The cost of insuring debt against a default has risen for various countries over the past few months, most notably Lebanon, Turkey, Pakistan, and Argentina.

Sources: Bloomberg, Reuters, FRED, IMF

Trade & Currency Concerns - International Update

Currency and debt concerns among emerging markets drove global volatility upward. Fiscal turmoil with Turkey and Argentina spread to other emerging economies as the fear of contagion rose.

A stronger U.S. dollar in addition to tariff tensions added to the uncertainty as emerging market currencies fell versus the dollar.

Russia, considered an emerging market, was also affected by sanctions imposed by the U.S. The sanctions are considered political yet may develop into more economic sanctions should relations falter. Russia’s currency, the ruble, has fallen over 16% this year versus the U.S. dollar.

Trade and tariff disputes continued to headline uncertainty throughout the global markets. Canada, Mexico and China were in the forefront of negotiations as the administration sought tariff relief for U.S. companies selling products overseas.

Sources: Dept. of Commerce, FRED

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.