Macro Overview

Financial markets were distraught during the third quarter as rising rates, inflation, and slowing economic activity hindered major equity indices. Dramatic tax cuts implemented in the U.K. stirred global financial currency markets with the British pound falling to historic lows. Fiscal policy reform is becoming a focal point as various international economies are poised to fall into recession.

The effects of Hurricane Ian on the insurance and property casualty industry may take months to determine. Preliminary estimates are expected to surpass $57 billion in property losses and damage, yet not as catastrophic as Katrina’s $125 billion in losses during 2005.

Affordability constraints from elevated home prices and rising mortgage rates continue to hinder housing nationwide. Consequently, mortgage volume for both purchased and refinanced loans fell to a 22-year low in late September due to increasing rates which are slowing mortgage activity.

Concerns surrounding the extent of the Federal Reserve’s strategy on raising rates affected fixed-income and equity markets in September. The Fed’s strategy to combat inflation by increasing the Fed Funds rate has been one of the most ambitious in decades. The Federal Reserve increased short-term rates again in September with the Fed Funds rate reaching a target range of 3% to 3.25%.

Sources: Federal Reserve, FreddieMac, Mortgage Bankers Association, Treasury Dept., Bloomberg

Stocks Endure Difficult Third Quarter - Domestic Equity Overview

Equities across the board were down in the quarter ending September 30th, as the market continues to react to global turmoil and the Fed’s aggressive interest rate spikes. Sectors that held up the best relative to other sectors included biotechnology, healthcare services, and oil/gas, joined by banks, semiconductors, and healthcare equipment.

Various equity analysts believe that the current rallies in equities are bear market rallies with little or no fundamental strength. Optimistically, certain sectors are establishing more attractive valuations as prices have receded.

Sources: S&P, Dow Jones, Bloomberg

Short-Term Bond Rate Remain Higher Than Long-Term Bond Rates - Fixed Income Review

Rising rates are being compounded by the Fed’s suspension of buying U.S. Treasuries and mortgage bonds on the one market. Along with the Fed’s current increase in short-term rates, the additional pressure on the fixed-income market has exacerbated the rapid rise in interest rates.

Short-term Treasury bond yields remained higher than longer-term maturities in September, known as an inverted yield curve. The 2-year Treasury yield finished September at 4.22% while the longer-term 10-year Treasury yield was at 3.83%.

Sources: U.S. Treasury, Bloomberg, Federal Reserve

Housing Affordability Series 1 of 2: Rising Mortgage Rates Deter New Buyers - Housing Overview

The 30-year conforming mortgage rate has a profound effect on the prices of homes and the rate at which interest is collected on mortgages. This rate is increasing, which has an inverted effect on home prices, causing them to drop for the first time in over a decade.

Between July and June of 2022, home prices experienced their first monthly drop since March of 2012. This ended a decade-long surge of rising home prices by falling to -0.44% from June to July of 2022. The cause of this is high mortgage rates.

Mortgage rates, as of late September 2022, have reached 6.7%. This is the highest they have been in over 16 years and have not reached this level since July 2006. When mortgage rates are at such high levels, they can deter new homebuyers, as potential buyers do not want to purchase a home on which they have to pay such high interest. Thus, sellers are forced to drop their home prices to look more favorable to buyers, but such high mortgage rates still end up making most houses more expensive than they were months ago when home sale prices were relatively higher.

Currently, 66% of Americans are homeowners, which is down from 2004 highs of nearly 70% but still on the rise from 2016 lows of 63%. However, these mortgage rates are expected to drop the homeownership rate yet again as an increasing amount of potential buyers are dissuaded from purchasing a home now and instead look to rent and wait until mortgage rates drop.

Sources: U.S Census Bureau, S&P Dow Jones Indices, Freddie Mac, Federal Reserve Bank of St. Louis

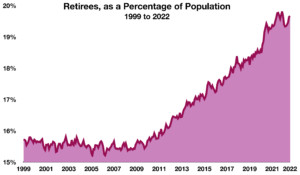

Retirees Make Up an Increasing Part of the Population - Retirement Trends

Since the early 2010s, the share of the U.S. population made up of retirees has been growing at a fairly constant rate, yet saw a spike since the beginning of the pandemic. In just the first year of the pandemic, an additional 1.3% of the population was made up of retirees- which is 3.6 million people.

In comparison, the average annual growth rate from 2010 to 2020 was just 0.3% per year. Had this pace continued, the Kansas City Fed states that the number of retirees would have expanded by 1.5 million rather than the actual 3.6 million retirees. The increased rate generated over 2 million additional retirees.

This increase, however, is not attributed to the commonly held perception of retirement where employed people transition into retirement. According to the Kansas City Fed, this increase in the number of retirees is due to the decrease in the number of retirees who decide to come out of retirement and rejoin the workforce. So, for many retirees, deciding to go back to work sounds much more unappealing than it did in the years leading up to the pandemic.

Compared to rates before the pandemic, current employment-to-retirement and retirement-to-unemployment rates have remained constant, whereas a drop-off has been seen in the rates of unemployment-to-retirement and retirement-to-employment. This portrays that around the same number of people are entering retirement from the workforce or starting to look for a job during retirement, while fewer people are finding a job after retirement.

Many retirees are still generally considered young enough to rejoin the workforce and have rejoined the workforce since the pandemic has calmed down this past year. From February 2020 to June 2021, 0.7 million people under the age of 60 retired, 0.5 million between the ages of 61-67, and 1.6 million between the ages of 68-75. Over 250,00 A large amount of these groups can return to work, which may lead to an increase in retirement-to-employment rates in the future.

Sources: Kansas City Fed, U.S. Census Bureau

The Fed’s Continuous Increase Of The Fed Funds Rate - Monetary Policy

The Fed Funds Rate, which is controlled by the Federal Reserve Board (also known as the Fed), is the interest rate at which banks charge each other to borrow money. This year, the Fed has continued to aggressively increase the rate.

The effects of increasing the Fed Funds Rate are more expensive borrowing costs and reduced demand for borrowing money. By increasing the rate, the Fed hopes to pacify rising inflation, as the U.S. is currently experiencing the highest inflation rate observed since 1981.

In March of this year, the Fed began its increase of interest rates. Before then, the rate was effectively at close to 0% between April 2020 and February 2022. As of September 21st, the rate has a target range of 3% to 3.25%, which means the rate has risen 3% in just 7 months. This is the largest increase made by the Fed in a single year since 1982. Based on this, the Fed Funds Rate would reach 4% to 4.25% by the end of the year.

Sources: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis, Federal Reserve Bank of New York

Unemployment Claims On The Rise - Labor Market Overview

Unemployment claims reached their highest level since late November 2021, and have steadily increased throughout the year. As of the week ending on August 6th, the job market saw initial unemployment claims rise to 262,000. This was an increase of 14,000 claims from the previous week’s 248,000 claims and an increase of over 30,000 claims from just 6 weeks prior. This gradual increase in unemployment claims is emerging as uncertainty over the economy expands. Many sectors, specifically tech and real estate, are experiencing stagnated hiring and even layoffs.

With a volatile stock market and a slowing economy, technology companies are easing and even freezing hiring and in some cases conducting layoffs. Optimistically, layoffs are not at the high levels they were during the pandemic, but unemployment claims have been steadily increasing. This could foreshadow more uncertainty in an economy that has begun to slow down.

Sources: U.S. Employment and Training Administration, Federal Reserve Bank of St. Louis

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.