Macro Overview

Equity markets defied the historically negative month of October with equity indices moving higher despite ongoing trade dispute uncertainty and growing concerns of global economic headwinds.

Major domestic and international equity indices rose in sync as interest rates remained low worldwide, driving assets into stocks. Monetary policy that prompted rate cuts by central banks around the world are expected to provide stimulus and bolster global growth as the cost to borrow remains low.

Some concerns do exist surrounding a global economic slowdown, with attention on economic data becoming a focal point for analysts and economists. U.S. equities have continued to perform as a result of an accommodative monetary policy driven by the Federal Reserve and consistent consumer demand which have buoyed stock valuations.

Trade talks between the U.S. and China have continued to roil markets as inconsistent messages regarding any progress on trade discussions have not yielded any formal trade agreements. The ongoing trade dispute has brought about revisions to economic growth estimates by economists and international organizations such as the International Monetary Fund (IMF) and the World Trade Bank.

Bond yields rose in October, a possible indication that growth dynamics are propelling some prices and interest rates higher. Economists view a slight rise in rates optimistically due to healthy economic forces driving expansion. Treasury bond yields saw modest increases in October, with the 10-year Treasury yield rising to 1.69% on October 31st from 1.68% on September 30th.

The Federal Reserve cut its key interest rate for the third time this year. The most recent cut in late October was preceded by two cuts earlier in the year, the first in July and the second in September. The Fed hinted that no further rate cuts were anticipated unless weaker economic data warranted additional cuts.

The Treasury and the Federal Reserve are closely monitoring the possibility of year end volatility when banks are hesitant to part with cash reserves, which affects money markets. Short-term rates briefly spiked in September as the cost for banks to borrow cash against Treasuries jumped. Banks actively participate in Fed driven strategies that indirectly affect short term rates and liquidity in the bond markets.

Following several failed attempts to formally extract Great Britain from the European Union (EU), also known as Brexit, the prime minister of Great Britain has given the vote back to the people of Great Britain with an election on December 12th. British voters originally voted on exiting the EU in 2016, but with no formal agreement ever having been reached between the British government and the EU. The vote is expected to garner enormous attention from other EU countries considering an EU exit vote.

Sources: Federal Reserve, U.S. Treasury, EuroStat

Bond Yields Stabilize - Fixed Income Overview

The Federal Reserve injected additional amounts of funds into the overnight lending markets, also known as the repo market, in October. The move served to dampen concerns that a repeat of volatility that hit markets in December 2018 would occur again.

The Federal Reserve cut interest rates for the third time this year but signaled that it would not cut them further unless economic growth slowed amid concerns.

Yields on government and corporate bonds remained stable in October as expectations of economic growth and a pause to further rate cuts stabilized bond markets. Bond prices have risen since the beginning of the year, with government and corporate bond yields still hovering near record low levels. Bond prices move in the opposite direction to yields.

Sources: Federal Reserve, U.S. Treasury

Stock Indices Move Higher In October - Global Equity Review

Both domestic and international equity markets advanced in October, lodging new highs for various indices. The S&P 500 Index and the Nasdaq Index both closed at record levels as of November 1st. Developed and emerging market indices propelled higher in October buoyed by a continued low rate environment and a weaker dollar.

Volatility, as measured by the CBOE, (Chicago Board Options Exchange), Volatility Index, or VIX, fell to a near annual low in October, as subdued risk concerns dominated.

The technology and health care sectors were the top performing large cap sectors in October, with energy as the worst performing sector in the S&P 500 Index. Market analysts are seeing a shift or rotation towards value from growth, reminiscent of a more cautionary environment.

Sources: S&P, CBOE, Bloomberg

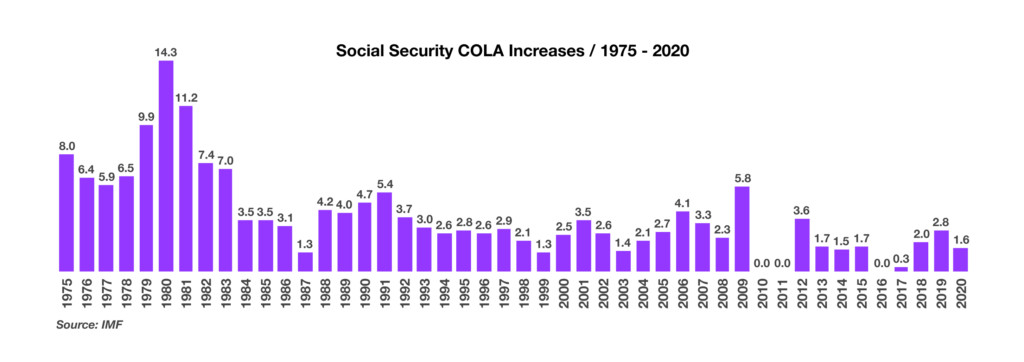

Social Security Payments Increasing By 1.6% - Retirement Planning

Social Security recipients are due to receive a modest increase in benefit payments payable in 2020. But for many recipients, the increase in payments will go towards higher Medicare costs. The increase will affect over 63 million Americans receiving Social Security benefit payments.

The Social Security Administration announced a 1.6% increase in benefit payments effective in late December 2019 for disability beneficiaries and in January 2020 for retired beneficiaries. The 1.6% increase is slightly less than the increase of 2.8% for 2019.

Many are concerned that the 1.6% increase may not cover expenses that are rising at a faster rate, including other essential items such as food and housing. The establishment of Social Security occurred on August 14, 1935, when President Roosevelt signed the Social Security Act into law. Since then, Social Security has provided millions of Americans with benefit payments. The payments are subject to automatic increases based on inflation, also known as cost-of-living adjustments or COLAs, which have been in effect since 1975. Over the years, recipients have received varying increases depending on the inflation rate. With low current inflation levels, increases in benefit payments have been subdued relative to years with higher inflation.

Over the decades, Americans have become increasingly dependent on Social Security payments, however, for some Americans it may not be enough to rely on Social Security alone. Unfortunately, Social Security is a major source of income for many of the elderly, where nine out of ten retirees 65 years of age and older receive benefit payments representing an average of 41% of their income. Over the years, Social Security benefits have come under more pressure due to the fact that retirees are living longer. In 1940, the life expectancy of a 65-year old was 14 years, today it’s about 20 years.

By 2036, there will be almost twice as many older Americans eligible for benefits as today, from 41.9 million to 78.1 million. There are currently 2.9 workers for each Social Security beneficiary, by 2036 there will be 2.1 workers for every beneficiary.

Source: Social Security Administration, https://www.ssa.gov/news/cola/

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.