Macro Overview

Geopolitical tensions in the Middle East along with the ongoing invasion of Ukraine in Europe, is escalating defensive positioning in the markets as funds are being diverted to less volatile asset classes. Domestic and international equity indices retracted in April, as markets reacted to the tensive environment.

Iran’s attack on Israel prompted a recalibration among financial markets worldwide as the demand for government bonds, gold, the dollar and cash all rose. Shipping and transportation routes may become broadly affected as conflict in the region spreads to other geographic areas.

Many analysts believe that inflation is being kept elevated not by consumer demand, but by price increases as companies struggle to maintain margins. Consumers meanwhile are finding it more difficult to identify less expensive substitutes. The Fed has nearly no influence on easing non consumer driven inflation since its main policy tools, such as the Fed Funds rate which affects short term interest rates, targets consumer expenditures.Three areas are seeing the most inflationary pressures, auto insurance, rents, and health care premiums.

Stronger than expected employment data has led the Federal Reserve to wait on cutting rates until data proves otherwise. Economists view resilient labor conditions as inflationary because it allows consumers to continue to spend throughout the economy. A slow down in hiring and employment gains is signaling a cooling labor market, which is what the Fed is ideally seeking in order to start cutting rates.

The Federal Reserve carefully tracks lending activity and releases its finding via the Loan Officer Opinion Survey each month. April’s release revealed that banks and lenders continue to tighten on credit lending, making it more difficult for consumers to borrow on mortgages, credit cards, automobiles, and lines of credit. The tighter lending environment is also affecting small and mid size businesses that require credit for ongoing operations.

Of all of the developed country central banks worldwide, the Federal Reserve is the only one yet to embark on lowering rates. Japan, Germany, the U.K and the European Union, have all initiated rate reduction policies. Many analysts believe that the Fed is very close to start reducing rates, especially as other central banks have already done so.

The lack of supply of new homes across the country along with ongoing demand for existing homes has contributed to the average age of a residential home in the U.S. to be 40 years old. Home buyers are spending more on updating and modernizing older homes as newer homes have become increasing difficult to find. A lack of supply along with elevated home prices continues to make it challenging for younger families.

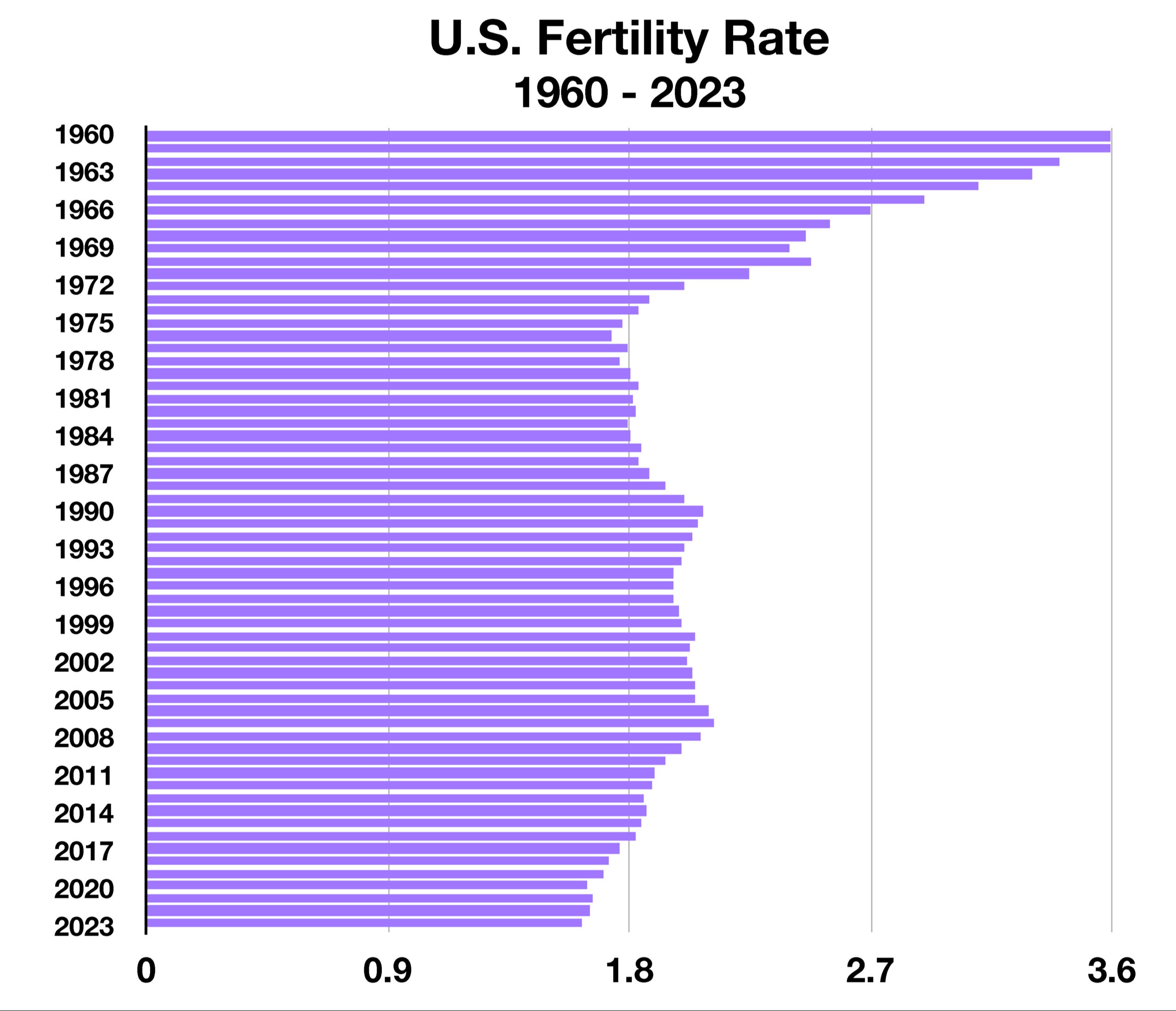

The fertility rate in the United States fell to 1.62 births per woman in 2023, a 2% decline from a year earlier, according to data from the U.S. Department of Health and Human Services. The current fertility rate is the lowest rate recorded since the U.S. government began tracking the data in the 1930s. The U.S. fertility average is below the global average of 2.3 births per woman as of 2023 data.

Sources: U.S. Dept. of Health, Federal Reserve, Treasury Dept., S&P, Bloomberg

Geopolitical Tensions Challenge Stocks In April - Domestic Equity Overview

Domestic equity indices in April experienced the most volatility since September 2023, as the Dow Jones Industrial Average, the S&P 500, and the Nasdaq all saw pullbacks in April. Ten of the eleven sectors of the S&P 500 Index posted negative returns in April, with the utilities sector posting the only gain for the month. Emerging market indices posted some gains relative to developed economy indices, yet still struggled through the month.

Sources: S&P, Dow Jones, Nasdaq, Bloomberg

Yields Remain Stubborn As Fed Waits - Fixed Income Overview

Bond yields and interest rates stalled in April, as the Fed announced that it wasn’t yet ready to begin reducing rates. Geopolitical tensions in the Middle East also affected Treasury bond yields, as demand increased for Treasuries driving prices higher and yields lower. The Fed’s resistance to reduce rates still affected yields ion April, with the 10-year Treasury yield ending April at 4.69%, up from 4.20% at the end of March.

Shorter term maturity and longer term maturity bonds are starting to see more similar yields, meaning that the yield curve is flattening. Analysts view this as a signal that rates may start to settle from their recent increases, and with a possible shift in economic activity.

Sources: Treasury Dept., Federal Reserve

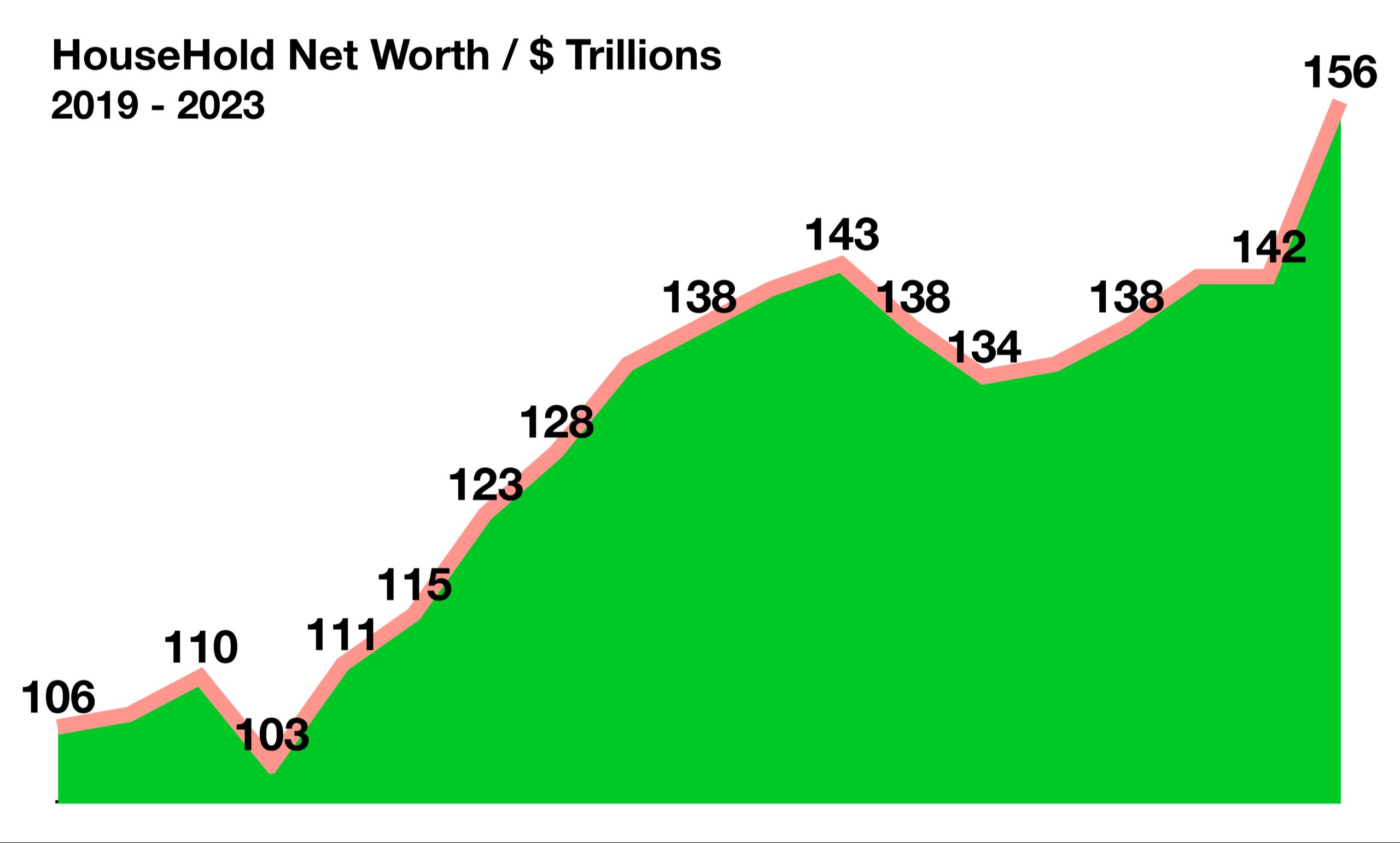

It’s The Wealth Effect That Keeps Everyone Spending - Consumer Economics

Even as inflation and higher rates have been an ongoing hinderance, consumers remain resilient and continue to spend. The reasoning behind the confidence and tenacity of consumers is believed to be what is known as wealth effect, which is the change in spending that accompanies a change in perceived wealth.

An increase in the wealth effect has been a result of the increase in real estate and equity values, which has created a sense of wealth thus prompting consumers to spend more. Real estate and equities have pushed the level of household net worth up an astonishing $11.6 trillion over the past year, encouraging consumers to spend more out of current income. Some analysts and economist relate this scenario to what occurred in the late 1990s.

Economists view wealth effect as more of a psychological phenomenon where an increase in home and stock values are perceived as a justification to spend more as thought it was an increase in income. In actuality, the increase in asset values may not be sustainable and may even result in a devaluation, erasing confidence and spending motivation for consumers.

Source: Federal Reserve Bank of St. Louis

Why Small Businesses Are So Important To The Economy - Domestic Economy

The country is composed of millions of small businesses from home-based one person consultants to hair salons and manufacturing companies. As defined by the SBA’s Office of Advocacy, a small business has less than 500 employees and operates independently, not under the control of another entity.

As of 2023, the SBA acknowledged that there were 33.3 million small businesses in the U.S., 22 million of which were individually operated with no employees other than the owner. At 49.2%, nearly half of the nation’s workforce is employed by a small business, representing roughly 120 million employees.

Small business employment suffered a massive set back during the pandemic, losing 8.6 million jobs in the second quarter of 2020 according to the U.S. Labor Department. Remarkably, small businesses recouped 4.9 million jobs between March 2021 and March 2022, accounting for roughly 70% of all new jobs nationwide.

Department of Labor data revealed that woman made up over 43% of small business owners in 2023, representing a significant portion of business owners across the country in various industries. Home health and personal care are projected to see the largest employment gains for small businesses over the next few years. An aging U.S. population along with a growing demand for health care workers continues to create a dire need for qualified employees.

Sources: Labor Department, BLS, SBA

Why Homeowners Insurance Costs Have Risen - Property Insurance Update

Homeowners nationwide are grappling with surging insurance costs and worse, coverage cancelations. Insurance companies are becoming much more defensive as claims for property damage have soared over the past few years. Damage resulting from hurricanes, tornadoes, flooding, fires, and other natural disasters have led to dramatic increases in policy premiums nationwide.

Hurricane and severe storm damage in Florida has led to expensive homeowners insurance premiums, while wild fire damage in California has prompted several insurance companies to cancel existing policy owners and deny coverage to new applicants. Premiums can vary dramatically among different geographic areas, and can also change quickly following numerous claims and increased risk factors. According to the Insurance Information Institute, the average homeowners insurance premium nationwide is over $2000 annually as of the end of 2023. Insurance underwriters are paying closer attention to changing weather patterns and extreme conditions caused by natural phenomenons.

Source: Insurance Information Institute

U.S. Fertility Rates Drop To Lowest Level On Record - Demographics

Prosperity and growth of a country is contingent on the health and expansion of its population. A measure of growth which eventually leads to a population demanding food, clothing, medicine, and other necessary goods is the fertility rate.

Most of the highest fertility rates in the world are found in emerging regions of Africa and the Middle East, where mothers are giving birth to as many as seven children. Fertility rates are lower among developed countries such as Germany, Japan, and the United States, where average ages are above 35.

U.S. fertility rates fell to their lowest level since the U.S. government started tracking data in the 1930s. The most recent data as of 2023 shows that fertility rates fell to 1.62 births per woman in 2023, a 2% decline from a year earlier. The drop is believed to be attributed to demographics, lifestyle changes, and economic constraints.

Many large multi-national corporations employ economists and demographics specialists to better determine what products and services may be optimized in various regions and countries as dictated by population growth. Agricultural companies, for example, tend to cater more food products and farming equipment to emerging countries made up of a younger population. This is so because statistically, younger people within a growing population eat more than older people.

A shift in demographics also creates a shift in the financial and labor markets, as older more mature populations provide less growth as well as a limited workforce. The younger emerging populations not only provide future growth, but are also a source of workers for growing economies.

Sources: CIA World Fact book, U.S. Dept. of Health

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.