Macro Overview

The Federal Reserve decided to leave rates unchanged in February, igniting concerns among the financial markets that interest rates may not fall as soon as many had expected. Larger than anticipated inflation data and resilient employment is deterring the Fed from lowering rates too soon.

The Consumer Price Index (CPI) revealed that inflation was running at 3.1% for the past year as of January, down from 3.9% in December. Some analysts believe that it may be too soon for the Fed to determine as to when it will lower rates, even though inflation seems to be alleviating.

A global recessionary environment is evolving, with recent economic data showing that the U.K. and Japan have both fallen into a technical recession. Global growth forecasts by the International Monetary Fund (IMF) indicate a broad pullback in economic expansion among various countries worldwide.

Interest rates remained stubborn in February as Treasury bond yields rose slightly across all maturities, known as a shift up in the yield curve. Larger than expected inflation data as well as the Fed’s hesitancy to lower rates, drove bond yields higher in February.

Three Federal Reserve officials announced that the pace of rate cuts by the Fed will be contingent on yet to be released economic data. Fed officials differed as to when any rate cuts would materialize, two suggested “later this year” while one estimated this summer. The Fed’s most significant factors when determining any reduction in rates remain inflation, employment, and economic growth.

The growing interest and recent rise in Artificial Intelligence (AI) has reinforced a lingering belief that the domestic economy has begun to shift from an industrial economy to a digital economy. Economists believe that such a transformation, should it ever completely occur, might take decades to evolve.

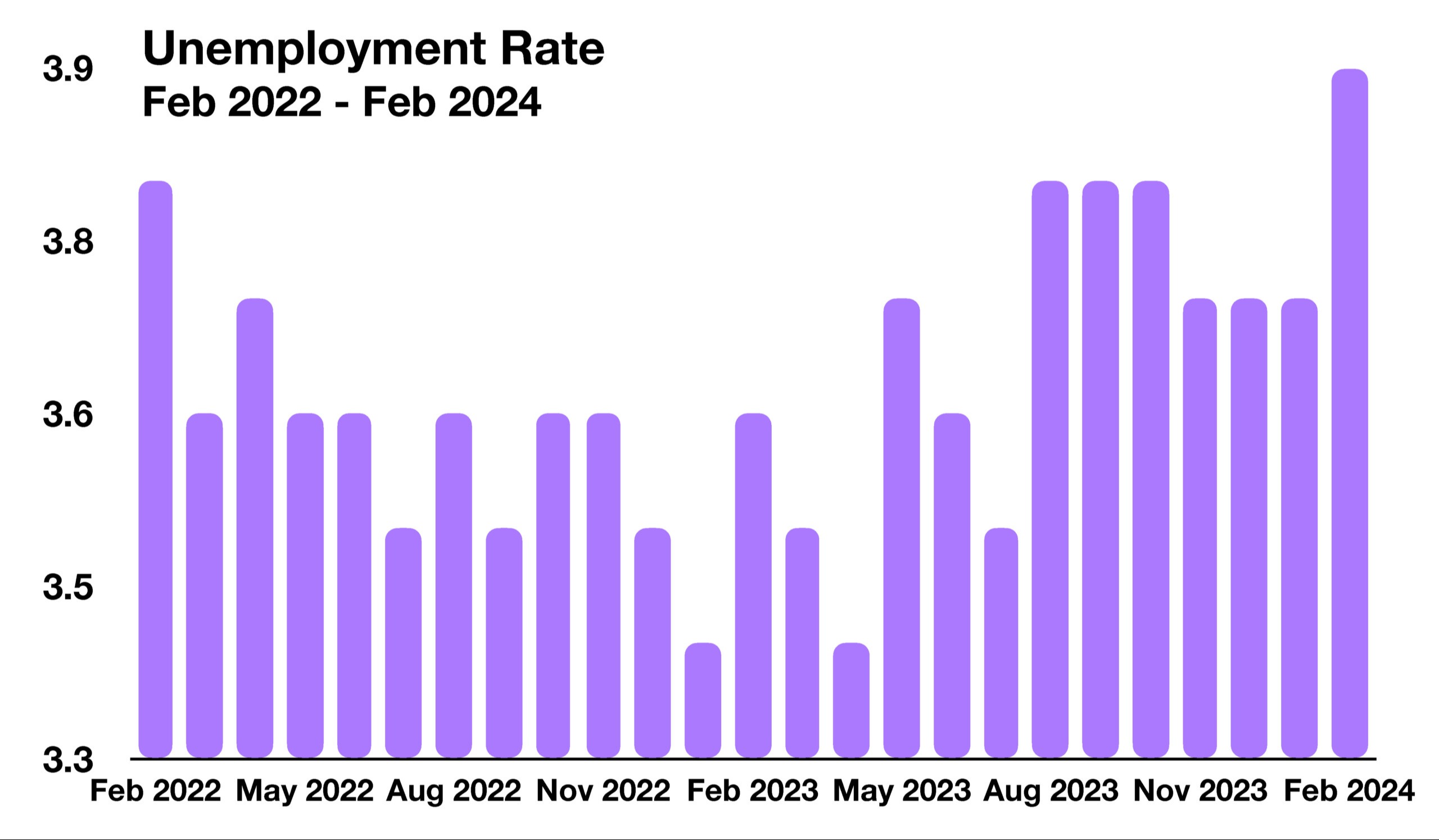

Unemployment rose to the highest level in two years, hitting 3.9% in February, as reported by the Department of Labor. Wage growth also slowed from the previous month, possibly signaling a cooling labor market as perceived by economists.

Requirements for large banks to hold more capital are being proposed by the Federal Reserve. A proposal to boost bank capital by 19% is seen as a preparation for a possible retraction in economic activity as well as defaults among bank holdings. Regulators including the FDIC and the Office of the Comptroller of the Currency support the heightened capital requirements. Banks argue that the additional capital requirements would increase lending costs and tighten loan availability for consumers and businesses.

According to data released by the Bureau of Labor Statics, the past year has seen an increase in the purchase of lottery tickets and an increase in gambling. Some analysts believe that the proliferation of online gambling and lotto purchases is facilitating an increase in speculative consumer behavior.

Sources: Federal Reserve, Labor Dept., BLS, IMF

Stocks Advance In February - Domestic Equity Overview

All eleven sectors of the S&P 500 Index posted positive results in February, with technology, financial, and healthcare making up the largest sectors of the index. The Dow Jones Industrial Index and the Nasdaq also posted positive gains in February.

The technology sector now accounts for roughly 30% of the S&P 500 Index, a level not seen since the early 2000s. This means that recent gains in the tech sector have elevated valuations thus making up a larger proportion of the index. Some analysts view this dynamic as a disparity and imbalance in the equity markets.

The average price of an individual stock in the S&P 500 is now $204.28, with some 73% of them (or 281 stocks) selling for more than $100 and 9 trading for more than $1,000 as of the end of February. Compared with 40 years ago, when the average price was $39.06 and approximately 4%, or 9 stocks, traded for more than $100, and with no stocks were over $1,000.

Sources: S&P, Reuters, Bloomberg

Rates Remain Hesitant in February - Fixed Income Overview

Interest rates rose slightly across all maturities in February, resulting in what is known as a shift up in the yield curve. The Fed’s resistance to lower its key rate, the Fed Funds rate, resulted in markets expecting elevated rates for a longer period. Communications from Fed officials indicate that rates may not be reduced until the summer or perhaps even the fall.

The benchmark 10 year treasury bond yield ended February at 4.25%, up from 3.95% at the beginning of the year. The shorter term 2 year treasury bond, yielded 4.64% at the end of February, up from 4.33% at the beginning of January. The slight increase in both maturities led to an increase in rates on some consumer loans during the month.

Sources: Treasury Dept., Federal Reserve

Unemployment Ticks Up & Wage Growth Slows - Labor Market Update

The unemployment rate rose in February to 3.9%, the highest level in two years. The Department of Labor also reported that wage growth slowed in February from the previous month. The Department made substantial revisions in February to previous data, clarifying the slow down in wage growth more clearly. Wage growth in February decreased significantly from the beginning of the year in January, surprising various analysts and economists. One of the Labor Department’s substantial revisions included data showing that the economy had added 353,000 positions in January, yet later reported that the number was actually 229,000.

Data tracked by the Labor Department also includes who acquired and lost jobs. The Department identified that native born Americans with a job fell by 881,000 over the past year to 129.3 million, while foreign born workers with a job rose by 1.5 million to 31 million over the same period.

Sectors experiencing employment gains include healthcare, government, and food services. Of concern to some analysts is that employment gains have been primarily concentrated in various lower paying positions. Some argue that the recent employment and wage data may be signaling a slowdown in the job market along with cooling wage gains across multiple industries. Economists perceive these labor market dynamics as indicative of a slowing economic environment.

Source: Department of Labor

Consumer Loans Are Falling - Consumer Finance Behavior

Outstanding loans among consumers have been falling since October 2022, reflecting a drop from auto loans to credit card balances. Such data can be viewed differently, either as a positive or negative result of economic circumstances and consumer sentiment.

A number of variables determine loan activity among consumers, including loan approval, income, sentiment, and need for a loan. Historically, an increase in loan activity has been optimistic as increased income and sentiment among consumers leads to heightened loan requests. Also affecting loans recently are loan approvals, where banks and finance companies have increased lending requirements among consumers and businesses, making it more difficult to obtain a loan. A drop in wages or an increase in living expenses may also deter consumers from taking out loans, as financial constraints make it challenging to qualify and repay loans. The Federal Reserve tracks and analyses loan activity and data for signs of consumer hesitation and sentiment, which eventually affects the economy, since over two-thirds of GDP is contingent on consumer expenditures.

Sources: Federal Reserve

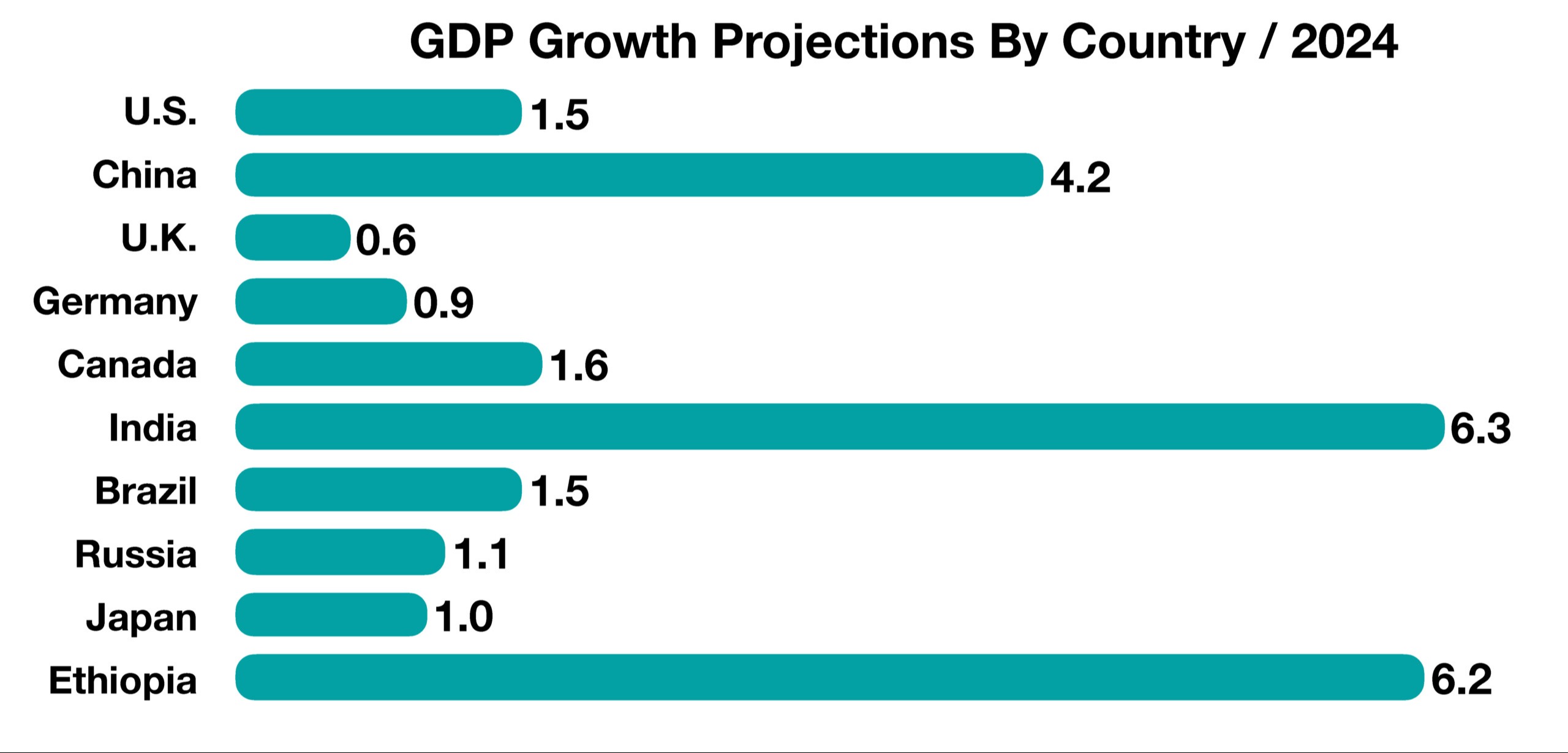

Recession Looms Internationally - Global Economy

Global growth projections and changing business activity internationally, are indicating a global pullback in economic activity, with an evolving recessionary environment.

Each year, the International Monetary Fund (IMF) releases a forecast of global GDP growth by country. Projections for 2024 are lower than they have been in prior years, with a noticeable pullback with developed economies. The IMF projects that both emerging markets and developed economies are projected to grow by 4% in 2024. GDP growth estimates for the U.S. are conservative, at 1.5%, while projections for China are at 4.2% and 6.3% for India.

France, Japan, and the U.K. have slipped into technical recessions, defined by two consecutive quarters of declining GDP data. Germany is also running the risk of falling into a technical recession as well. Germany and Japan are critical economic components of the global economy, with vast manufacturing and production, representing over $3 trillion of total global exports. A persistently weak Japanese yen has helped maintain Japanese exports, yet is inflationary for consumers in Japan especially when buying imported goods.

Economic data coming from China reveals that housing prices have been falling and property developers have been defaulting on their debt over the past year, possibly affecting consumer sentiment and expenditures in the country.

Thus far, the U.S. has avoided a recessionary environment, even as other developed economies have begun to falter. International trade activity with other countries, as well as domestic consumer expenditures, will be critical factors in validating any retraction in the nation’s economy.

Sources: CIA World FactBook, IMF

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.