Macro Overview – February 2017

A change in sentiment was prevalent throughout the markets as new rules and regulatory reversals began to take effect. Volatility rose as markets tried to discern President Trump’s policies.

Equity markets propelled to new highs in January as optimism fueled U.S. equities, sending the Dow Jones Industrial Average to a new milestone level of 20,000. The S&P 500 Index and the Nasdaq Composite Index also reached new highs during the month.

Executive orders undertaken by the President were able to derail several rules signed into law by the Obama administration, yet fiscal policy initiatives proposed by President Trump such as tax cuts and tax reform need Congressional approval. The Congressional Review Act (CRA) will allow the Republican led Congress to reverse a number of regulations enacted by the prior adminustration.

Among President Trump’s first actions as president was to withdraw the U.S. from the Trans-Pacific Partnership, strengthen border parameters with Mexico and temporarily disallow certain immigrants from entering the U.S. Two highly contested oil pipeline projects were granted the ability to advance, the Keystone Pipeline and the Dakota Access pipeline.

Pharmaceutical companies became a Presidential target, as President Trump approached drug makers to lower their prices and manufacture their products in the U.S. The President’s agenda of repealing portions of the Affordable Care Act may also affect premium and medical costs.

Brexit became more of a challenge in January as the highest court in the U.K. ruled that Prime Minister Theresa May must seek a parliamentary vote in order to continue on with exiting the EU.

A continually strong dollar is creating headwinds for U.S. multinationals which post a large portion of their earnings from over sea’s sales. A weaker dollar would be beneficial to U.S. exporters making their products less expensive internationally.

Fiscal concepts presented by the President may encourage companies with ample cash to invest in capital rather than buying back their own stock or issuing heftier dividend payouts. A lagging key component of GDP has been capital spending.

The National Federation of Independent Business released their survey of small business optimism, which soared 7.5% to its fifth highest level in over 40 years of survey results.

President Trump nominated 49-year old Neil Gorsuch for a lifetime job on the U.S. Supreme Court. Gorsuch, the son of a former Reagan administration official, is the youngest nominee to the nation's highest court in more than a quarter century, and could influence the direction of the court for decades.

Sources: Fed, Eurostat, NFIB, Dow Jones, S&P

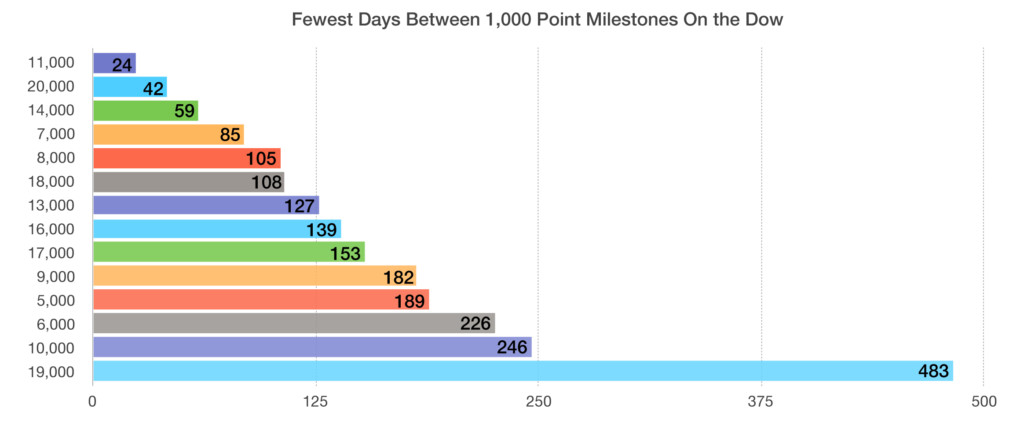

Dow Jones Reaches 20,000 – Domestic Equity Update

The Dow Jones Industrial Average hit the milestone 20,000 mark in January. The 120-year old index took 103 years to reach 10,000 in March 1999, then another 18 years to reach 20,000 in January 2017. The move from 19,000 to 20,000 took just 42 trading days, the second fastest 1,000 point gain in history for the index. The single fastest 1,000 gain occurred during the dot com boom in 1999 when the index jumped from 10,000 to 11,000 in only 24 days. Two other notable equity indices also reached new highs in January, the S&P 500 and the Nasdaq.

Equity markets pulled back at the end of January as uncertainty surrounding various administrative policies and some disappointing corporate earnings fueled a retraction of major indices. Earnings were mixed in January as earnings were reported for various companies across different sectors.

A number of industries that have been laggards for the past 4 to 8 years have now become candidates for growth and expansion: oil & gas drillers, metal & glass containers, fertilizers & agricultural chemicals, tankers, and mining.

A common complaint about stock market growth has been the fact that most companies found it easier to simply issue debt at low interest rates and buy back their own stock, rather than investing in capital with the constant tide of regulatory resistance discouraging expenditures.

Sources: Dow Jones, S&P

International Markets React – International Update

Markets throughout the world reacted to the various orders and actions executed by President Trump with caution, meaning that foreign companies and governments need time to see how such proposals would unfold.

The dollar’s strength continues to weigh on emerging markets that essentially compete with the dollar in attracting capital.

The euro staged a minor comeback at the end of January, as Brexit became more of a challenge when the highest court in the U.K. ruled that Prime Minister Theresa May must seek a parliamentary vote in order to continue on with exiting the EU. Britain’s expected exit from the EU has devalued the British pound since the passage of the vote to exit the EU.

Asian markets were in a quandary as the U.S. withdrew from the Trans-Pacific Partnership (TPP), a free trade agreement among 12 countries (including the U.S.) signed in 2016. Comprised mostly of Asian countries, the TPP excludes China and consists of countries bordering the Pacific Ocean.

Sources: EuroStat, Bloomberg

Increase In Bond Yields Stall - Fixed Income Update

Demand for bonds increased towards the end of January following a pull back in equities. The rise in bond demand brought bond yields lower from their elevated levels earlier in the month. An inverse relationship exists with bonds, as bond prices rise, bond yields fall.

Analysts believe that the anticipation of increased infrastructure spending and government borrowing might lead to a significant boost in Treasury borrowing, which could push up borrowing costs for the government in the form of higher interest rates.

Remarks by Fed Chairperson Janet Yellen signaled that the Fed intends to increase rates throughout 2017, contingent on economic and employment growth. Janet Yellen’s term as Fed chief ends in June 2018, allowing the President to appoint a new Fed boss then.

Sources: Federal Reserve, Bloomberg

Why GDP Growth Was Lackluster For 8 Years – Domestic Economy

A key component of GDP growth has been lagging for years, as a lack of incentives for companies to invest in capital has been an issue.

Many believe that economic growth since the financial crisis in 2008/2009 has been driven primarily by the monetary stimulus efforts enacted by the Federal Reserve. The Quantitative Easing programs, aka Q.E. 1 & Q.E. 2, provided tremendous liquidity for nearly eight years as the Fed bought debt and placed it on its balance sheet.

The problem is that what the Fed did was considered a form of “artificial stimulus”. Rather than investing in capital equipment for long-term economic growth, companies instead borrowed money at historically low rates via issuing debt, then bought back a portion of their stock. This in turn helped send stock prices higher without any tangible economic growth strategy in place. As this transpired, GDP growth lagged and companies basically became complacent with anemic rates of growth.

Source: BLS

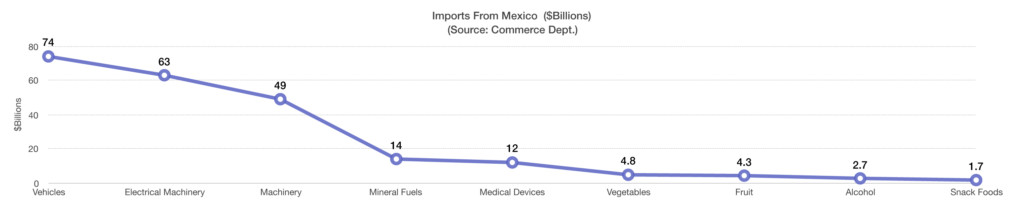

What The U.S. Imports From Mexico – Trade Overview

The Trump administration has proposed a 20% tariff on imported products from Mexico in order to better balance the trade deficit with the country. Some argue that imposing such a tariff would make certain imported products more expensive for American consumers.

The U.S. imported over $21 billion worth of vehicles from Mexico in 2016, with auto parts accounting for the single largest type of product imported from Mexico valued at over $51 billion in 2016, making the automotive industry an integral component of trade with Mexico. Interestingly enough, exports headed from the U.S. to Mexico are primarily for use in the automotive industry, with machinery, fuels, and plastics making up the largest portions.

Agricultural and food products imported from Mexico, such as tomatoes and beer, totaled over $21 billion in 2015, the most recent data available.

Sources: Dept. of Commerce, BLS

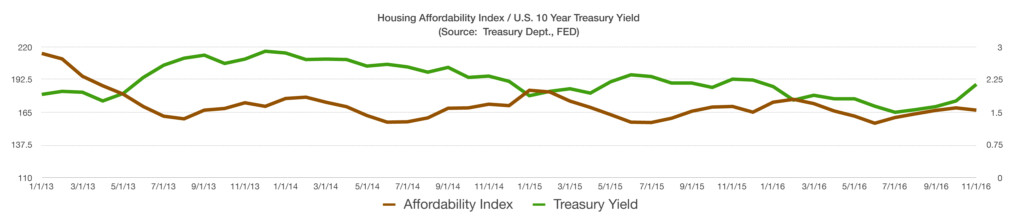

Homes Become Less Affordable As Rates Move Up – Housing Market

The recent rise in rates has led to a drop in the Housing Affordability Index as tracked by the Federal Reserve. Both existing and new home sales slowed towards the end of 2016 as a rise in rates pushed mortage rates higher. Rising interest rates tend to increase the cost factor when purchasing a home with a mortgage loan.

The two most feasible methods of raising the Affordability Index is by either having an increase in wages or by having a drop in housing prices. Historically, home prices tend to fall much faster than wages rise, since pay raises take time.

The Housing Affordability Index is negatively correlated to the 10-year Treasury Bond yield, meaning that as yields rise, the Affordability Index declines.

Source: St Loius Federal Reserve Bank

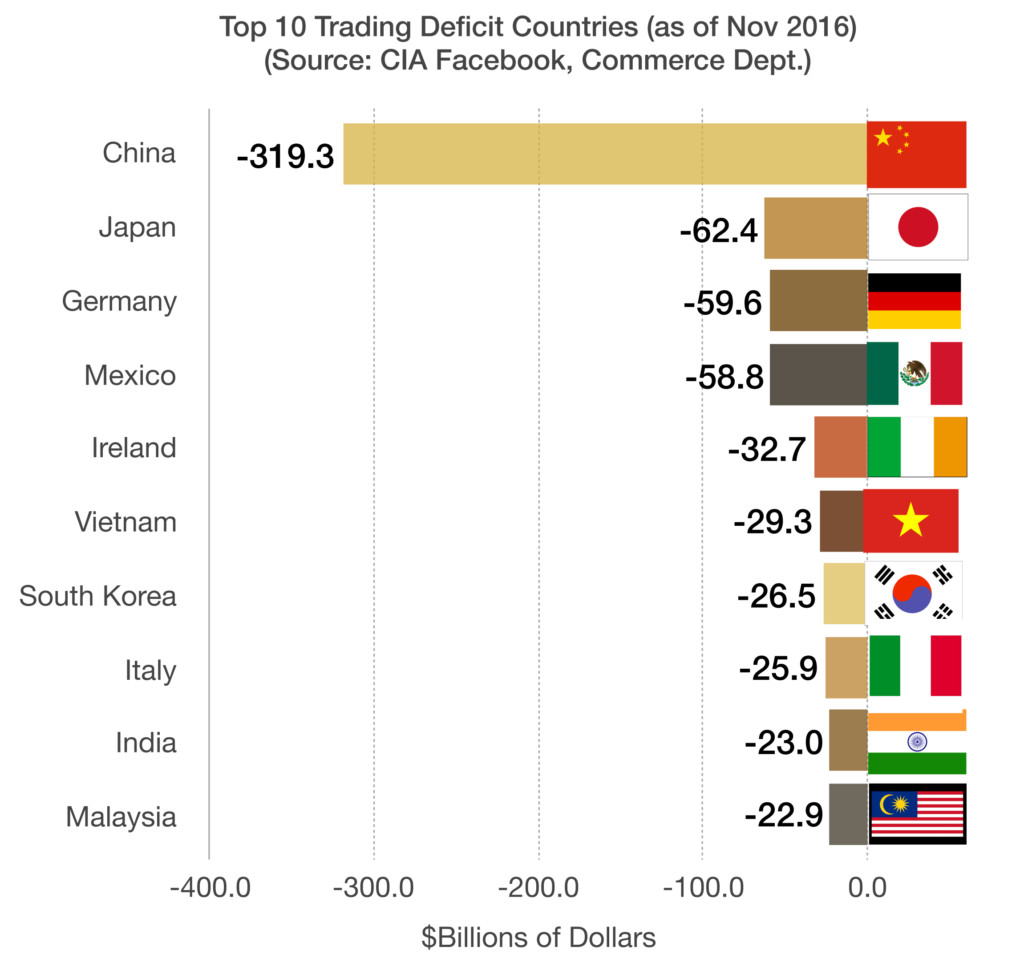

Largest Trade Deficits With U.S. By Country – International Trade

The United States has provided a tremendous consumer market for countries all over the world, with an abundance of products imported from a variety of areas.

Growing U.S. consumer demand over the decades along with advanced electronic manufacturing facilities in China and throughout Asia, have given American consumers cheap products. Ambitious consumer behavior has created a trade deficit with China of over $319 billion dollars, followed by smaller deficits with Japan, Germany and Mexico.

The current deficits with Japan and Germany are primarily comprised of automobiles and machinery, while the deficit with China mostly consists of electronics.

Appreciation of the U.S. dollar versus other major currencies has made foreign products relatively cheap for American consumers, including automobiles, computers, and televisions.

Sources: CIA Factbook, U.S. Dept. of Commerce

*Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.