Macro Overview

Global markets shifted positively in November as the Federal Reserve signaled that further rate hikes were less likely as economic conditions and inflation cooled. Stocks and bonds both advanced in November, following the expectations that the Fed may be on track to finalize its rate increase initiatives. Various fixed-income analysts even project interest rate cuts by the Federal Reserve as early as March 2024.

Numerous economists and analysts are encouraged that the Fed may have decided to ease its fight against inflation due to the most recent Consumer Price Index (CPI) release indicating that inflation is easing. November CPI data revealed that inflation rose at the slowest pace since 2021, with the CPI rising at 3.2%, down from 7.1% a year ago in November.

There is also a growing consensus that the Fed may be able to achieve a soft landing by easing rates slowly and avoiding the risk of recession. The U.S. economy has thus far been incredibly resilient to the Fed’s rate hikes, which have been hawkish over the past year. The Federal Reserve has communicated that it is carefully monitoring the effect of heightened interest rates on consumers and the economy. Some analysts believe that if the economic environment slows more than the Fed expects, then a transition to lowering interest rates might eventually be executed by the Federal Reserve.

Government data disclosed that domestic economic growth, as measured by Gross Domestic Product (GDP) grew at an annual rate of 5.2% in the third quarter of 2023, up from 2.1% in the second quarter of the year, according to the Bureau of Economic Analysis. Since the Federal Reserve tracks GDP growth for inflationary pressures, fourth-quarter data for 2023 will be critical in determining the Fed’s conclusive decisions on the direction of interest rates.

The price of nearly all major commodities has fallen this year, indicative of lessening inflationary pressures as global economies experience slower economic expansion. Commodities including copper, lumber, natural gas, and crude oil have all declined for the year so far, both domestically and internationally.

The number of job openings nationwide has been declining all year, with over 11.5 million open positions in January 2023, falling to 8.7 million in October, as revealed by the most recent government data available. Companies in various industries including technology and leisure, have begun scaling back on hiring and some have even implemented layoffs. Economists view a wavering labor environment as an indication of a possible economic slowdown.

Federal income tax rates are set to increase slightly in tax year 2024, with increases across most income brackets for both single and married taxpayers. The standard deduction for married couples filing jointly for tax year 2024 rises to $29,200, an increase of $1,500 from tax year 2023. Some increases are indexed for inflation while others are set by legislative reform.

Sources: Federal Reserve, Treasury Dept., BEA, Labor Dept., IRS, St. Louis Fed Bank

Equity Indices Appreciate In November As Rates Fall - Equity Market Overview

Equity indices advanced in November as expectations that the Fed has ceased rate hikes with the possibility of rate reductions as early as March 2024. International and domestic indices climbed as optimism for improved earnings rose for most sectors. Interest-sensitive sectors including technology and financials experienced the largest advances in November. Small capitalized companies also benefited as lower rates reduced borrowing costs. The Dow Jones Industrial Average, the S&P 500 Index, and the Nasdaq all rose in November alongside bond prices that also rose during the month.

Sources: Dow Jones, S&P, Federal Reserve

Bond Yields Fall As Bond Prices Rise In November - Fixed Income Update

Bond prices rose in November with Treasury and corporate bonds posting record gains. The resulting drop in bond yields was encouraging for the overall market as the expectations of possible Fed rate cuts early next year prompted optimism. Investment grade, high yield, and government bonds all rose in November encompassing all major sectors of the fixed-income spectrum. The Treasury Department also sold less debt than expected in November causing a shortage of supply for global investors.

The yield on the 10-year Treasury bond fell to 4.37% at the end of November, down from 4.95% at the end of October. The average rate on a 30-year fixed-conforming mortgage fell to 7.22% in November, down from 7.79% in October. Many bond analysts and economists expect a gradual downturn in interest rates over the coming months.

Sources: Fed, FreddieMac, Treasury Dept.

Year-End Tax Planning Activities – Tax Planning Overview

As year-end approaches, the importance of gathering necessary tax items is essential. Even though not much may have changed since 2023, it is always clever to have accurate estimates and tax items prepared for 2024.

Employer Qualified Retirement Plans

Whether you are a self-employed individual or a W-2 employee, it is important to tally up any contributions that may have been made to your retirement accounts over the year. Most employer retirement accounts allow for year-end contributions until December 31st. So any additional contributions that you can make to a company-qualified plan such as a 401(k) or a 403(b) should be made before the end of the year. Its a good idea to estimate how much more you can contribute then, spread out the additional contributions between now and year end. The maximum employee contribution for tax year 2023 is $22,500.

Investment Portfolios

For investors that hold securities as various types of positions, it is important to identify any investments that may have either significant losses or significant gains, which should be realized before the end of the year. With the market being as volatile as it has been, it is also important to identify any investment positions that may yield some type of tax benefit before year end.

Alternative Minimum Tax (AMT)

Affecting more and more people every year, Alternative Minimum Tax (AMT) should be carefully considered when implementing tax planning strategies going into the new year. Originally enacted in 1969, AMT was never indexed for inflation, thus it continues to affect more and more taxpayers each and every year. AMT is essentially an additional tax on top of the standard tax tables. Theres a good chance that taxpayers taking significant deductions at the state and local levels (such as state tax-free municipal-bond income), claiming multiple dependents, exercising stock options, or recognizing a large capital gain for the year, may eventually be affected by AMT.

Sources: Tax Foundation, IRS

Why Cash Isnt Going Away Anytime Soon – Currency Overview

With the onslaught of popular electronic payment methods, cash still continues to be a primary payment method of choice. The average person still uses cash for transactions every month and in some cases will only use cash for certain purchases, according to an analysis by the San Francisco Federal Reserve Bank.

Various benefits for cash still exist, where credit cards or electronic payment forms just cant compete. The most compelling reason to use cash is the fact that it is anonymous, meaning that the person spending the money is invisible, relative to making a payment with a credit card or electronic method that can be tracked and identify whos spending.

The San Francisco Fed study found that the average person pays with cash about 23 times a month, more often than credit cards and electronic payment forms. Most cash transactions are used for purchases of under $25. The study also identified 18 to 24-year-olds prefer cash to other payment forms, maybe due to the lack of credit card access available to younger consumers and students.

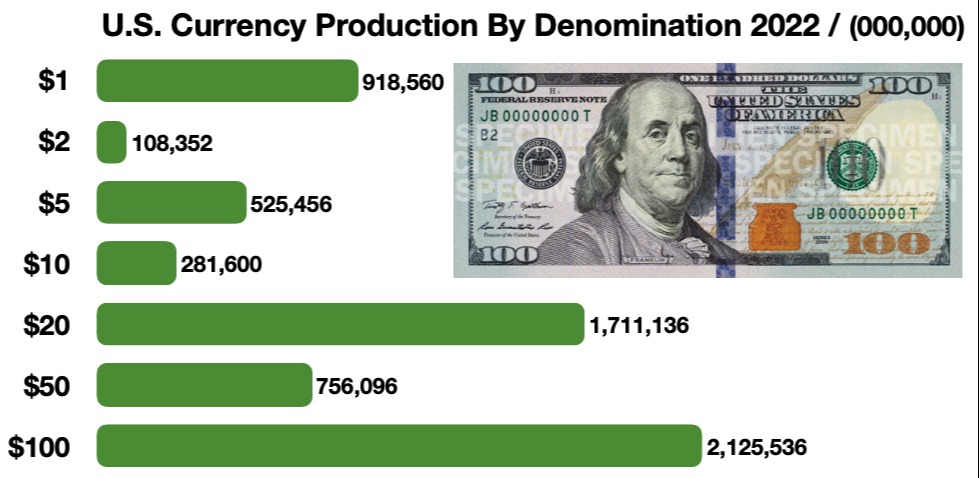

Of the various U.S. currency denominations in circulation, the 100-dollar bill is by far the most popular and the single most printed note. For the past two fiscal years (2022 & 2021) the 100 dollar bill has been the most produced note by the U.S. Bureau of Engraving & Printing, with over 2.3 billion individual 100-dollar bills printed in 2021, and over 2.1 billion 100-dollar bills in 2022.

Over 90 percent of currency printed by the U.S. Bureau of Engraving & Printing goes to replacing old and tattered bills already in circulation. Interestingly enough, rather than replacing old bills with new electronic payment forms, cash continues to be king.

Sources: San Francisco Fed, U.S. Bureau of Engraving & Printing

Why Gas Prices Rise Faster Than They Fall – Commodities Review

Consumers nationwide are frustrated at gasoline pumps as prices have leaped much more quickly than they have dropped. As the drop in gas prices has afforded more discretionary spending for consumers, it now adds to the uncertainty of where fuel prices might be headed.

A study released by the Federal Trade Commission (FTC) showed that gasoline retail prices rise four times faster than they fall after wholesale price changes. The dynamics behind the price conundrum is how much gasoline stations pay for fuel and how long it takes for them to sell that fuel before wholesale prices move higher or lower.

Competition is also a factor as one station may have bought an 8,000-gallon load of gasoline the day before the decline started, in which case they'll be even slower to drop their price since they paid a higher price. If a station isn't as willing to be competitive, it stalls other stations from dropping prices further. Stations aren't in the business of losing money, so they tend to resist dropping prices until another station does. That’s why there may sometimes be four stations on the same corner, yet selling the same grade of gasoline at different prices. Refineries, inventories, and delivery times also impact the price paid at the pump as these factors may vary from station to station.

The FTC study also found that in some places around the country, gasoline retailers sell at a loss when wholesale prices are high and then try to make up for that loss when prices go down. Retailers try keeping prices higher for as long as possible as the only way for them to make a minimal profit, or in some cases break even. Some stations are even willing to sell gasoline at a loss since some of these stations make most of their profit from attached convenience stores. If a sign boasting low prices draws drivers to the station, they're more likely to spend money in the store.

Interestingly enough, the FTC study identified that when prices are high, buyers search around to find a better deal. Immediately after prices go down though, buyers don't search as hard. This gives a cushion for the station owners to lower prices in smaller increments.

Sources: EIA. FTC

Travel To U.S. Continues To Rebound After Pandemic - Travel Industry Update

The travel industry in the United States is enormous, with over $887 billion spent every year on lodging, food services, transportation, and amusement. The most is spent on dining, with over $209 billion going to restaurants and other food service entities nationwide. Hotels and retail stores also capture a generous portion of what travelers spend.

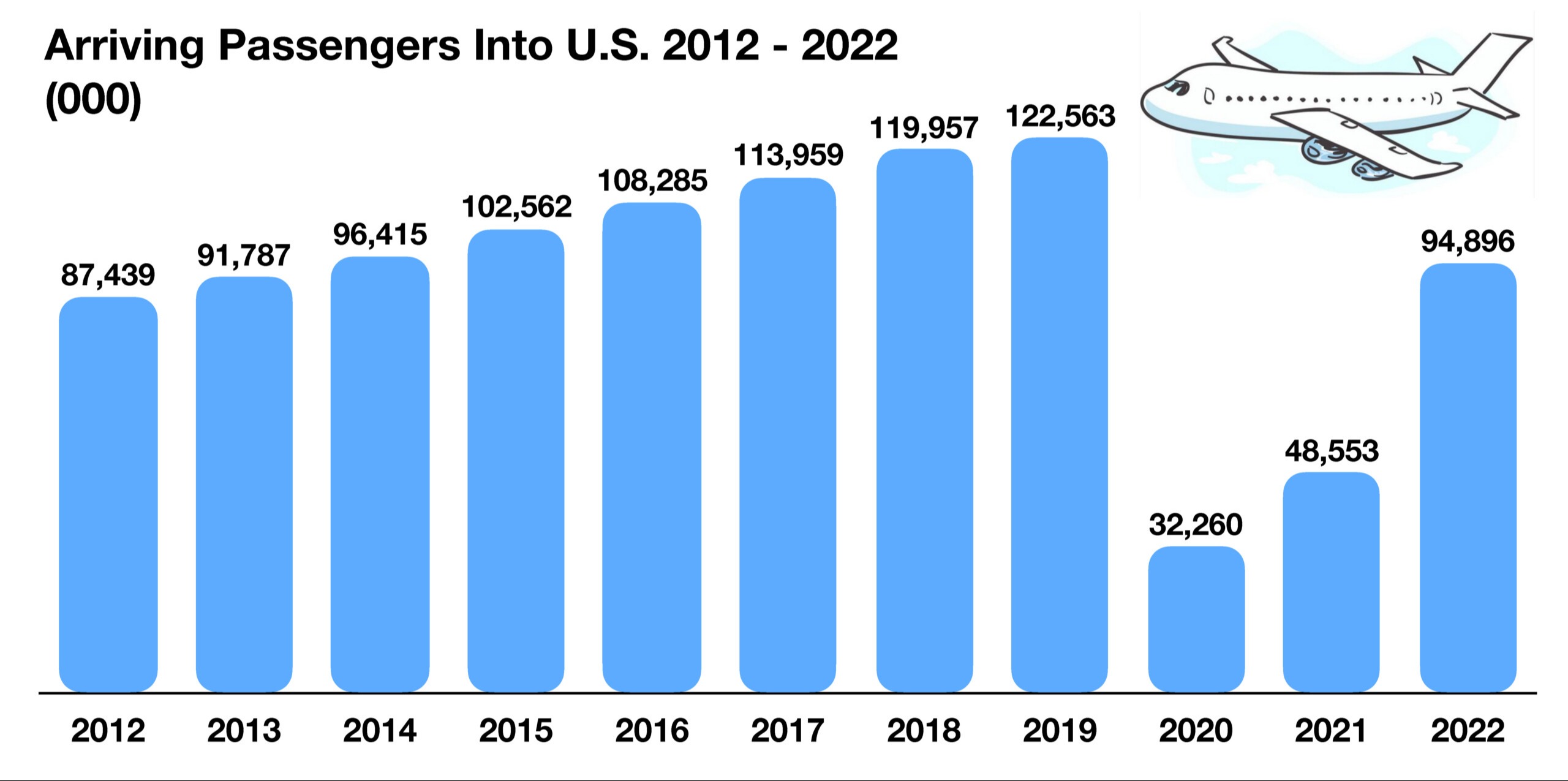

Well-maintained roads and secure facilities throughout the country afford Americans the ability to travel confidently across the states. As do U.S. citizens, foreign travelers also find the United States a safe and easy country to visit and vacation in. In 2022, the U.S. had over 94 million international arrivals into airports and seaports. Of these, the majority were directly from Canada and Mexico, with the remaining arrivals from various countries overseas. The U.S. Travel Association calculates that every international traveler to the U.S. spends $4500 on their stay, which averages about 17 days.

Since the attacks of September 2001, it has become more difficult for foreign travelers to enter the United States, as fewer visas are issued and fewer foreign passports are allowed into the country. These security procedures have curtailed some travel to the U.S. but have not dampened the desire to visit the United States.

In aggregate, the travel industry generates over $2 trillion in economic activity, which includes direct spending, taxes, and jobs. Nearly 15 million jobs are supported by the industry, producing over $200 billion a year on wages earned by U.S. workers.

The average leisure traveler is age 47.5, which represents a typical consumer in their prime spending years and most likely with children. Thus, the majority of companies in the travel and leisure industries tend to create and focus their activities and themes around the desires and interests of this age group.

Source: U.S. Travel Association

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.