Macro Overview – December 2020

Equity markets responded positively to news that the availability of vaccinations was imminently close. Major equity indices reached new highs in November as elements of uncertainty eased with promising vaccine trials and finalized election results. With the election behind us, attention now turns back to the pandemic and its ongoing effects on the U.S. and international economies.

A lingering stimulus “cliff” has left millions of Americans in a quandary, as members of Congress failed to produce and pass a stimulus plan in order to provide essential benefit payments to struggling families. The hold up in extending existing benefits as well as establishing new benefits, is expected to be resolved by year end and effective early 2021.

Industries that saw the biggest job gains in November were also the same industries that lost the most jobs during the onset of the pandemic. Positions experiencing the largest gains are retailers, food services, and hospitality, which are also expecting to have the greatest challenges over the next few months.

The Center for Disease Control (CDC) as well as various health organizations estimate that the first COVID-19 vaccines will be available as early as mid-December in the United States. High risk individuals, including first responders and hospital workers will be among the first to receive vaccinations.

The anticipated disbursement of vaccines, which are expected in early 2021, are presumed to boost consumer sentiment and social mobility throughout the country. The widespread availability of COVID-19 vaccines, possibly from various pharmaceutical companies, are also projected to expand economic growth estimates.

Elevated unemployment continues to persist as large and small employers have scaled back on hiring and wages, creating ongoing frustrations for millions of unemployed workers nationwide. Fraudulent unemployment claims have become a growing issue, as the pandemic has lowered barriers to applying for and accessing benefit payments.

Absent any fiscal stimulus or year end pandemic relief funds, it is expected that the Federal Reserve will provide any essential stimulus by way of bond purchases. The Fed’s ambitious purchases of long-term bonds has kept long term rates low, helping to buoy consumer credit and the housing market.

World leaders met virtually for the G20 meeting which was hosted by Saudi Arabia in mid November. The primary objective on the agenda was the eradication of COVID-19 as well as facilitating distribution of vaccinations worldwide.

Sources: Federal Reserve, CDC, BLS, Dept of Labor, IRS, Social Security Admin.

Rates Rise Slightly In November - Fixed Income Update

Rates rose slightly in November, with the benchmark 10-year treasury bond yield approaching levels not seen in nearly six months. As the yield on the 10-year treasury neared 1%, fixed income markets embraced for potentially higher bond yields, which also means potentially lower bond prices. Historically low mortgage rates continue to bolster the housing market with record refis and purchases anticipated to continue through year end.

Sources: U.S. Treasury

Markets Head Higher in November - Equity Market Overview The combination of a finalized election, effective vaccine trials, and positive earnings from various sectors, drove equity indices higher in November.

The combination of a finalized election, effective vaccine trials, and positive earnings from various sectors, drove equity indices higher in November.

Analysts expect upcoming additions to the S&P 500 Index to produce added volatility with the index, creating demand for customized indexing, also known as direct indexing.

The rise of copper prices to a six-year high is an indication for market analysts that a global economic expansion may be in the making. Copper is a primary metal used worldwide in manufacturing, electronics, buildings, and infrastructure.

The Dow Jones Industrial Index reached the milestone mark of 30,000 in late November, bringing the index to new all time highs. The S&P 500 Index as well as the Nasdaq also saw higher levels in November, primarily driven by optimism surrounding promising vaccines.

Sources: Bloomberg, S&P, Nasdaq, Dow Jones

Medicare Coverage Heading Into 2021 - Retirement Planning

With open enrollment upon us, millions of Americans will be deciding on which, if any, changes to make to their Medicare coverage. The Open Enrollment Period for 2021 coverage is from November 1, 2020 to December 15, 2020. Coverage for any changes or new plans begins January 1, 2021.

Since Medicare doesn’t cover all medical expenses, the decision to buy supplemental insurance coverage or to obtain a Medicare Advantage Plan is important for millions of Medicare recipients.

Medicare Advantage Plans allow a recipient to get both Medicare Part A and Part B coverage. Medicare Advantage Plans are sometimes called Part C or MA Plans, and are offered by Medicare-approved private companies.

Medicare Supplemental Insurance or Medigap helps pay for gaps in coverage not paid for by Medicare. Even though Medicare does pay for many procedures and services, some remaining expenses such as copayments, coinsurance, and deductibles are covered by supplemental plans. Some Medigap policies also cover services that are not covered at all by Medicare, such as coverage while traveling abroad. So it’s worth shopping and determining what expenses are covered by the various supplemental insurance policies.

A recent change to Medigap eligibility over the past year is important to note. Medicare plans sold to people who are newly eligible for Medicare are not allowed to Cover the part B deductible. Because of this plans C and F are not available to people who are usually eligible for Medicare on or after January 1, 2020. If someone was already covered by plan C or F before January 1, 2020, that plan can be kept. If someone was going to be eligible for Medicare before January 1, 2020 but not yet enrolled, they may be able to buy one of the plans to cover part B deductible.

Source: medicare.gov

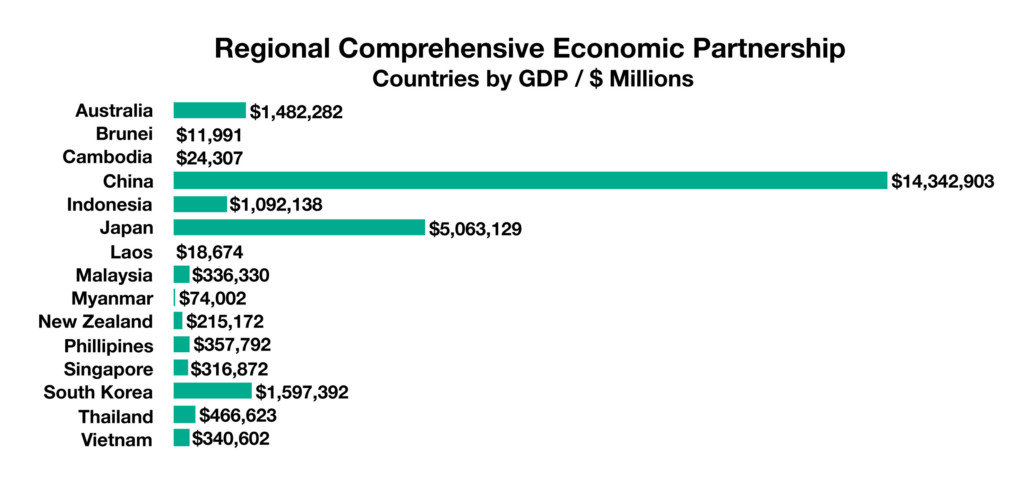

New Free Trade Agreement Doesn’t Include U.S. - Global Trade

For months, even before the onset of the COVID-19 pandemic in March, several countries were busy assembling trade agreements in order to facilitate and promote free trade. Asian countries were among the bulk of the agreements in the making, including both developed and emerging economies. This November, one of the long awaited free trade agreements was signed, the Regional Comprehensive Economic Partnership (RCEP), composed of Asian Pacific region countries.

Fifteen countries signed the RCEP, representing 30% of the world’s population and 30% of global GDP, making it the single largest trade block. The agreement is expected to take effect within two years, once it has been ratified by all 15 member countries. The RCEP was conceived in 2011 and has taken nine years to develop and establish.

The trade pact is the first free trade agreement among the countries of China, Japan, and South Korea, which include three of the four largest economies in Asia. Benefits of the agreement aim to reduce tariffs between the member countries, as well as facilitate the flow of goods among borders. Unlike other trade arrangements, the RCEP does not address environmental conflicts or labor union issues. In terms of nominal gross domestic product (GDP), China represents the largest economy of the 15 member countries. The U.S. opted not to be part of the RCEP, but intends to pursue other trade arrangements with various Asian countries.

Source: Regional Comprehensive Economic Partnership; Association of Southeast Asian Nations

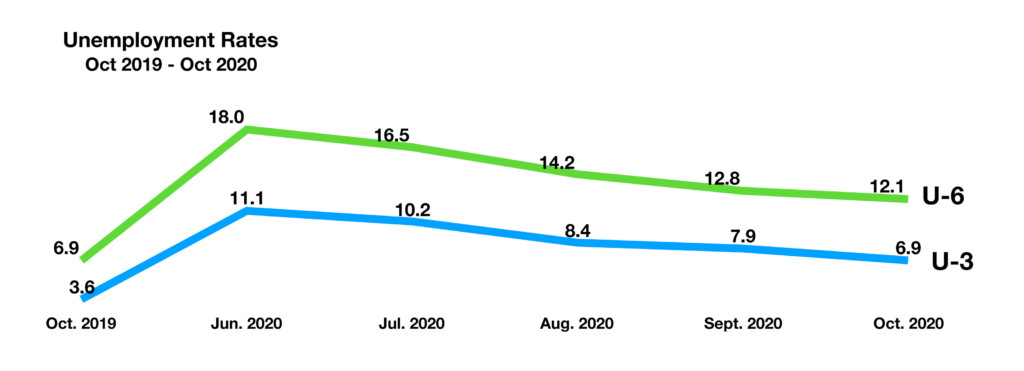

True Unemployment - Labor Market Overview

A closely followed economic statistic by economists and market analysts is the unemployment rate. In fact, the Department of Labor has numerous levels of unemployment rates that it compiles and reports. Of the various rates, the U-3 is known as the traditional or official rate, which came in at 6.9% for its most recent release. The U-3 rate is considered incomplete and inaccurate by many economists and analysts, since it only accounts for people actively seeking employment. Another available level of the unemployment rate is the U-6 rate, which is considered the true rate for unemployment. In addition to those people seeking employment, the U-6 rate also includes part time workers, underemployed workers, and discouraged workers. The U-6 rate is considered a more accurate assessment of the labor market and a true measure of unemployment. The most recent release for the U-6 rate is 12.1%, nearly double of the traditional U-3 rate.

Source: Bureau of Labor Statistics

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.