Macro Overview

A second wave of mandatory business closures that transpired throughout the country is expected to have more challenging ramifications for many employers than the first wave of shutdowns. The amount of stimulus funds and stimulus programs available to small businesses and individuals was substantial following the initial wave of closures and lock downs in March and April, yet benefits from a second stimulus batch is not expected to be as generous.

Tensions with China escalated as the U.S. State Department identified several Chinese spies accused of gathering sensitive data on coronavirus research as well as absconding with intellectual property. The latest occurrences leave trade negotiations with China in question, which had already been lingering since the pandemic began in March.

Equities rose higher in July driven by decent earnings for U.S. companies and the expectation of successful vaccine trials by several pharmaceutical firms. A rise in viral infections nationwide along with a rollback of re-openings by some states and cities pose a threat of halting a desperately anticipated economic growth spurt.

Congress sought to diffuse an income cliff as provisional government stimulus benefits expired at the end of July. A second stimulus plan is expected to be composed differently than its predecessor, but also targeted towards small businesses and the unemployed.

Gold and silver both reached new highs in July driven by global pandemic concerns and recent tensions surrounding the relations between China and the United States. Gold surpassed its previous high set in 2011 and silver achieved a six-year high.

GDP for the second quarter ending June 30th, shrank by an annualized rate of 32.9%, the lowest quarterly drop on record. A substantial drop was anticipated by economists and analysts. An economic slowdown was even more prevalent in Europe, where GDP within the EU fell by over 48% on an annualized basis.

The U.S. dollar came under pressure in July as it registered its worst monthly decline since September 2010. The decline, as measured versus other developed country currencies, is believed to be a result of surging U.S. government debt, dismal economic environment, and geo-political tensions.

The Centers for Disease Control and Prevention (CDC) reiterated the importance of re-opening schools in the fall for the benefit of families nationwide. The CDC noted that death rates among school-aged children are much lower than among adults, while the risks attributed to shut down schools affect social, emotional, behavioral health, economic well-being, and the academic achievement of children. Working families are finding it increasingly difficult to work and care for their children at home during the pandemic, especially with school closures.

Sources: CDC, Federal Reserve, BEA, State Dept.

Resilient Equity Market Advances In July - Domestic Equities Update

Equities advanced in July, led by the technology sector, which has remained resilient since the onset of the pandemic. The dollar’s tumble in July benefited large U.S. multinationals, whose products and services became more competitive while their earnings are primarily driven in the overseas market. The rebound in stocks from the lows of March, when the COVID-19 pandemic became official, has exceeded the expectations of both analysts and economists.

A consistent low-rate environment along with a weaker U.S. dollar bodes well for U.S. multinational companies, whose profits benefit from both low rates and a weak dollar. U.S. exports essentially become cheaper overseas, driving higher demand.

Sources: Bloomberg, Reuters, FRED

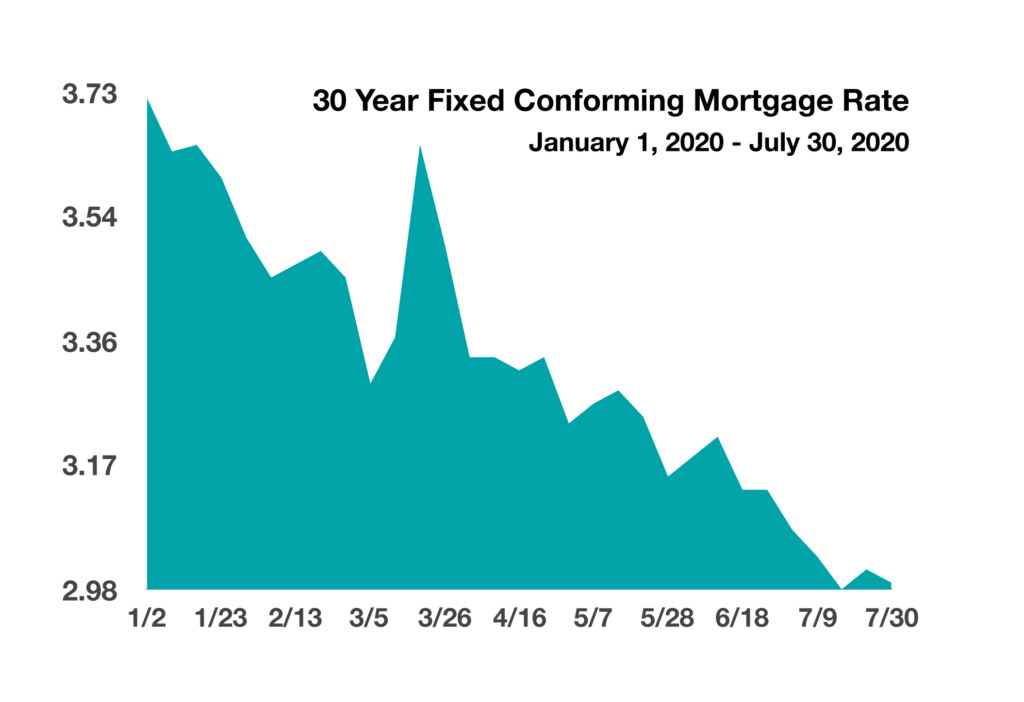

30 Year Mortgage Rates Drop to Record Lows - Fixed Income Overview

Continued low rates drove mortgage rates to their lowest levels ever, pushing the average 30- year fixed conforming rate to 2.99% in July as reported by Freddie Mac. Historic low mortgage rates are a buffer for the housing market, where continued high unemployment is expected to hinder loan approvals.

U.S. government bond yields fell across all maturities in July, with the benchmark 10-year Treasury yield reaching 0.55% and the 30-year Treasury yield falling to 1.20%. Economists view the higher yielding long-term bonds as a normal yield curve, indicating some inflationary expectations and future economic growth.

Sources: Freddie Mac, Bloomberg, U.S. Treasury

Gold Hits New High On Tensions - Commodity Update

Gold prices reached their highest level in July since 2011, eclipsing $1,897 an ounce. Nervousness surrounding the global pandemic, as well as geopolitical concerns between the U.S. and China, have steered buyers towards the precious metal, driving prices higher. The ultra-low interest rate environment has also made gold more appealing even though it offers no income, yet is still used as a store of value during times of geopolitical turmoil. Enormous stimulus efforts led by the United States is leading analysts to expect that inflation will eventually evolve, boosting the value of the metal due to its hedge against inflationary pressures.

Gold prices reached their highest level in July since 2011, eclipsing $1,897 an ounce. Nervousness surrounding the global pandemic, as well as geopolitical concerns between the U.S. and China, have steered buyers towards the precious metal, driving prices higher. The ultra-low interest rate environment has also made gold more appealing even though it offers no income, yet is still used as a store of value during times of geopolitical turmoil. Enormous stimulus efforts led by the United States is leading analysts to expect that inflation will eventually evolve, boosting the value of the metal due to its hedge against inflationary pressures.

For years gold has been a safe haven for investors looking to hedge against inflation, political crisis, and currency issues. The idea is that a country’s currency has a tangible backing, thus creating a sense of value that is accepted by the international markets. Gold has been for centuries, and continues to be, an accepted store of value worldwide.

For thousands of years, gold has been one of the most sought after metals in the world. It was first used as jewelry as early as 2600 BC in ancient Mesopotamia, what today is Iraq. Gold was introduced to dentistry in 600 BC, and has since then been introduced to various other applications. Several industries such as electronics, food, medical, and manufacturing all utilize gold in some fashion. Most notably, gold plays a significant role in the international monetary markets, where countries worldwide hold gold as a reserve. Holding gold as a reserve provides diversification among assets, economic security, and liquidity.

Gold is a unique asset in that it is no one else’s liability and, is not directly influenced by the economic policies of any individual country. Its status cannot, therefore, be undermined by inflation in a reserve currency country.

Sources: Congressional Research Service, Bloomberg

Shortage Of Coins Makes For No Change - Currency Dynamic

A reduction in the use of cash may have escalated a shortage of coins throughout the country. Retail stores and grocery stores across the country are experiencing a shortage of coins that has resulted from fewer coins being exchanged and spent since the onset of the pandemic.

In order to stimulate coin circulation, the U.S. Mint is asking Americans to use any spare change they may have to increase the circulation of coins. A dramatic drop in retail sales wasn’t the only cause of the shortage, but a drop in coin production at the U.S. Mint was also the culprit. Many federal employees for the U.S. Mint were shuttered from work as coronavirus infections spread throughout private and government work places.

Coins are used widely throughout the economy by consumers for a host of various products and services. Federal Reserve data from 2018 shows that 49% of goods and services under $10 were paid for in cash. Services such as laundromats traditionally require coins for payment.

The onset of the pandemic brought about a dramatic reduction in the use of coins, leading to a widespread shortage among retail stores, banks and even the Federal Reserve.

Sources: U.S. Mint, Federal Reserve

**Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.