Macro Overview – April 2017

Equity markets advanced during the first quarter as improving economic data supported gradually rising earnings. A steady and predictable path of anticipated rate increases this year by the Federal Reserve was well received by financial markets.

Domestic equity indices ended

The Fed hiked short-term rates as expected in March, on track with two additional hikes in 2017 with improving economic data validating the Fed’s

President Trump’s political capabilities are being tested as he needs to substantiate that he can formalize legislative arrangements rather than business transactions. The inability to initiate a bill to repeal the Affordable Care Act (ACA) created uncertainty as to whether or not future legislative ambitions would prove more challenging. In addition to resuscitating a health care bill, tax reform is expected to be President Trump’s next objective, which many expect easier to tackle since lower taxes are a common theme among the divided Republican party.

Two

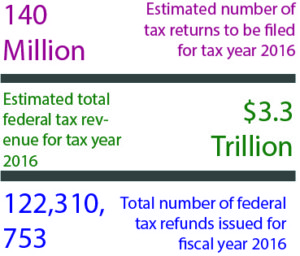

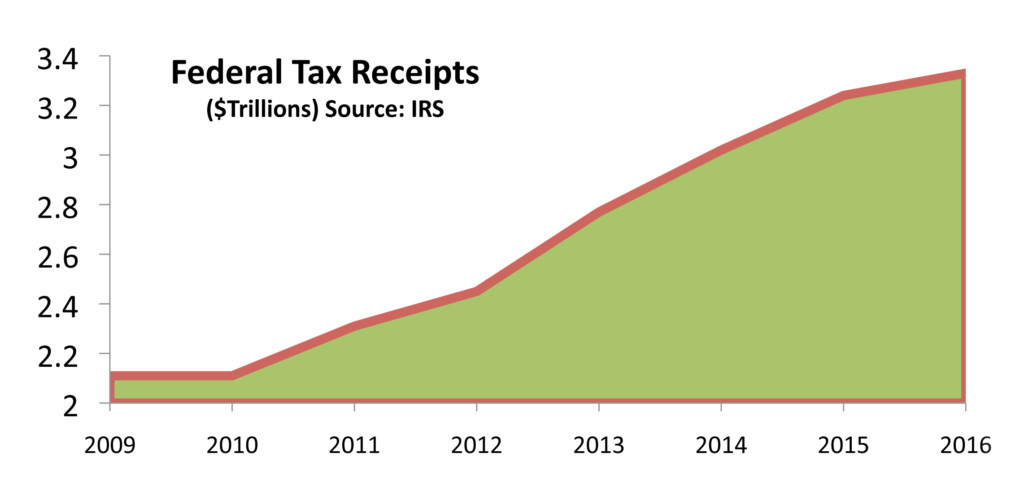

With tax season underway, estimates from the IRS show that over 140 million tax returns will be filed for the 2016 tax year with over $3.3 trillion in federal tax revenue.

Sources: Federal Reserve, Dept. of Commerce, Dow Jones, S&P

Generous First Quarter – Domestic Equity Update

The first quarter saw all of the major equity indices end positive, with the Dow Jones Industrial Index ending up 4.6%, the S&P 500 Index returned 5.5%, and the Nasdaq ended the quarter with a 9.8% gain. The S&P 500 index peaked on March 1st, ending lower at

Equity markets reversed an upward trend in place since the election, as the inability for House Republicans to agree on a revised

What was of interest regarding the positive outcome in the first quarter was that the market’s performance was not due to the Trump sector stocks that excelled following the election, which

On March 22nd, the Securities & Exchange Commission (SEC) adopted a rule to shorten the settlement period for securities from 3 business days to 2 business days. The SEC believes that a shorter settlement period will reduce certain credit, market, and liquidity risks. The new rule will take

Sources: SEC, Dow Jones, S&P

Rates On Track To

Rates retreated downward during the first quarter as growth prospects were alleviated even though the Federal Reserve raised rates in March.

Treasury bond yields rose in early March in anticipation of accelerated Federal Reserve tightening and then fell following a sense that the Fed may proceed with cautioned rate hikes due to possible lackluster economic data. The Fed increased its target on short-term rates (Federal Funds Rate) to 0.75-1.0% and signaled two more anticipated hikes in 2017.

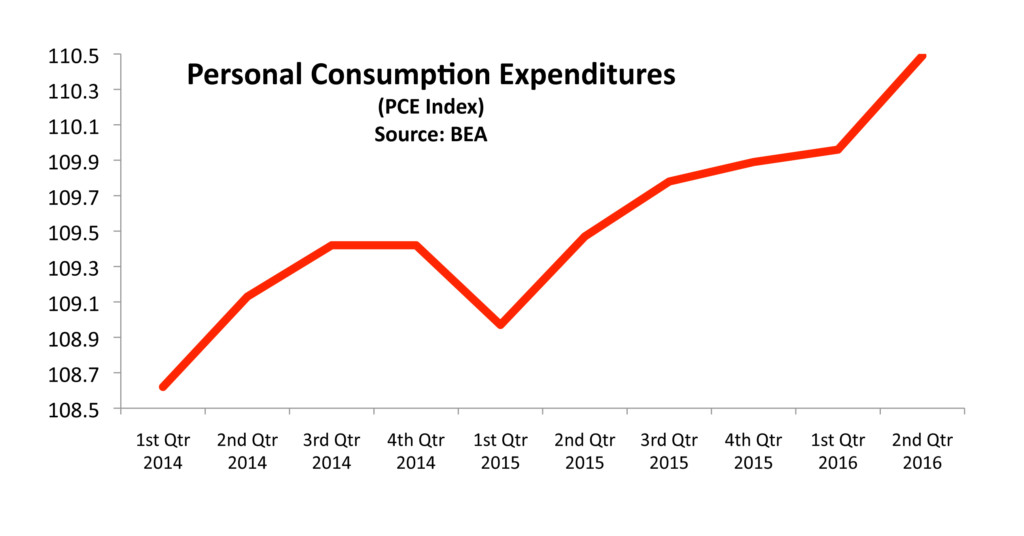

A jump in the Personal Consumption Expenditure (PCE) index to 2.1% has validated the Fed’s stance of continued rate hikes and an eventual winding down of its government and mortgage bond holdings on its $4.5 trillion balance sheet.

Sources: Federal Reserve, Reuters, Bloomberg

Inflation On Track For Fed Rate Hikes – Monetary Policy

A primary determinant for the Fed’s decision to raise rates is inflation. As part of its monetary policy objectives, the Fed had set a 2% target for consumer inflation as a trigger for sustained rate increases.

A closely followed indicator of inflation and what consumers pay for goods and services is the Personal Consumption Expenditures Index (PCE), which is compiled and released by the Commerce Department each month. The most recent data released shows that consumer inflation edged up 2.1% over the past year, marking its largest annual gain since March 2012.

A rising PCE is indicative of rising prices for consumers throughout the economy, in other

Ironically, even though inflation erodes the buying power of consumers, it is an essential ingredient for healthy economic growth. Inflationary pressures help elevate wages and income, allowing consumers the ability to spend more throughout the economy.Publish

Sources: Commerce Dept., Federal Reserve

Brexit Is Finally Underway – Euro Region Update

Ever since British voters decided to have Britain exit the European Union (EU) in June 2016, the process and timeline of the exit have been in question. This past month, British Prime Minister Theresa May triggered Article 50 which begins a two-year period of negotiations with the EU on exiting the union and establishing

Ever since British voters decided to have Britain exit the European Union (EU) in June 2016, the process and timeline of the exit have been in question. This past month, British Prime Minister Theresa May triggered Article 50 which begins a two-year period of negotiations with the EU on exiting the union and establishing

What has kept Britain from formally moving forward with its decision to exit the EU has been the delay in executing Article 50, which was never signed by the prior prime minister, David Cameron, and delayed by British courts on its applicability.

The execution of Article 50 comes at a time when other EU member countries are having elections with EU membership as a notable topic.

Here in the United States, triggering Article 50 is akin to having a U.S. state secede from the nation.

Sources:

Consumer Confidence On The Rise – Consumer Behavior

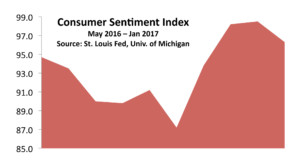

Two key measures of consumer confidence soared to levels not seen since 2000, helping to propel equities higher towards the end of the first quarter. Since consumer expenditures make up nearly 70% of Gross Domestic Production

A non-profit research group, The Conference Board, compiles and releases its Consumer Confidence Index each month, an indicator of consumer sentiment. In its most recent release, the Conference Board saw the largest increase in its index since December 2000. Another highly regarded index on consumer confidence is the Consumer Sentiment Index from the University of Michigan, which saw its largest increase in 17 years.

Sources: Commerce Department, University of Michigan, Conference Board

U.S. Tax Revenue – Fiscal Policy Review

With tax season upon us, the Federal government’s ability to tax comes into full force. The dynamics of tax revenue is a combination of economic prosperity, tax rates, and the existing population of taxpayers. Ongoing discussions surrounding tax rates have been a focus of how to increase tax revenue. However, the other two components include economic conditions and the number of individuals paying income taxes.

As new hires enter the workforce, either out of school or as immigrants, additional tax revenue is derived from their incomes. As economic conditions improve, companies may hire additional employees and eventually start to issue pay raises.

For the past 40

Sources: CBO, Tax Policy Center

45% of Americans Pay No Federal Income Tax – Fiscal Policy

An estimated 77.5 million Americans, identified as households, pay no federal income tax. The non-partisan, non-profit tax group known as The Tax Policy Center released income tax data it analyzed for 2015 and found that nearly half, about 45.3% of American households, paid no federal income tax in 2015. The Tax Policy Center estimates that the percentage of Americans that will not pay income tax for

Generous tax credits and low tax brackets for low-income earners allow minimal to no federal tax payments. The Tax Policy Center did find that these lower income households did pay their share of state, local, property, sales, and excise taxes.

Federal tax data for 2014 and 2015 showed the top 1% of taxpayers subject to a higher effective tax rate, averaging about 23%, seven times higher than taxpayers in the bottom 50%.

The ultra wealthy, also know as the top 1% of taxpayers, with annual incomes of about $2 million, pay about 44% of all of the federal income taxes in the U.S.

Source: Tax Policy Center/Washington D.C.

*Market Returns: All data is indicative of total return which includes capital gain/loss and reinvested dividends for noted period. Index data sources; MSCI, DJ-UBSCI, WTI, IDC, S&P. The information provided is believed to be reliable, but its accuracy or completeness is not warranted. This material is not intended as an offer or solicitation for the purchase or sale of any stock, bond, mutual fund, or any other financial instrument. The views and strategies discussed herein may not be appropriate and/or suitable for all investors. This material is meant solely for informational purposes, and is not intended to suffice as any type of accounting, legal, tax, or estate planning advice. Any and all forecasts mentioned are for illustrative purposes only and should not be interpreted as investment recommendations.